Monday 16th of March 2026 - Last Update: 12:36

")

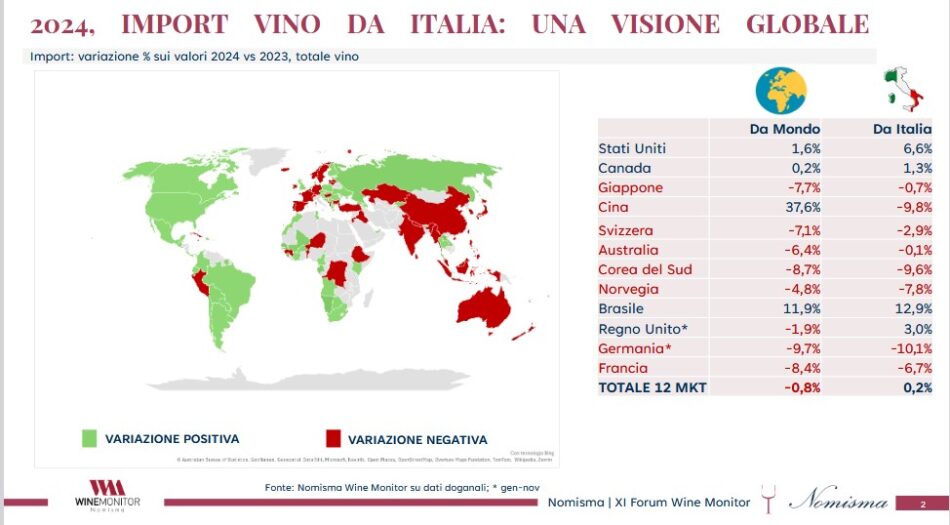

Back from the previous 12 months which have been certainly difficult, 2024 wasn’t the turning year at a global level for the wine world. Not a surprise, it has to be said, with euphoria “sentiment” of immediate post-Covid which vanished fast, and wine consumption which cooled in a quite difficult 2023. And, 2024 confirmed the negative trend, particularly considering international exchanges. It is sufficient to think that, among the 12 main import markets (which weigh for over 60% in world wine imports), positive variations for the US, Canada, China, and Brazil have been registered. But, in this framework, wine purchases from Italy grow more than the average, and the credit is mainly attributable to sparkling wines, which, in the same panel of 12 markets, register a +4.8% of value export against an aggregated average of -5.1% with peaks of +11% in the Usa, of 10% in Australia, and of 9% in Canada.

These are some of the main facts highlighted by Forum Wine Monitor No. 11, which occurred today, in live streaming, from Bologna, and which saw the alternation of detailed studies about wine market by experts of Team Wine Monitor, and of NielsenIQ (in the person of Eleonora Formisano, Sales director Smb & Global Snapshot Italy) with authoritative speeches by the entrepreneurial world such as those of Igor Boccardo, ceo Tenute Leone Alato-Genagricola, Carlo De Biasi, dg Agricola San Felice (Gruppo Allianz), and Massimo Romani, ceo Argea.

“Sadly - highlighted Denis Pantini, agri-food responsible Wine Monitor of Nomisma - the main import markets closed 2024 with a further drop, and those who went in countertrend underpin still suffering wine consumption such as in the case of the Usa, or of China, where the rebound of 38% of imports is entirely attributable to the return of Australian wines after they were banished by Chinese government in 2021 with a superduty of 218%”. A return that allowed Australian wine export to close 2024 in growth by 30% compared to the previous year, when, on the contrary, it underwent a drop of 10%. And who didn’t manage to recover from the drop in 2023 was French wine, which, overall, lost another 2.4% in value of exported wines (after -2.7% of the previous year).

The framework, regarding 2024 import, at a world level, sees the Usa at +1.6% (+6.6% from Italy), Canada +0.2% (+1.3% from Italy), Japan -7.7% (-0.7% from Italy), China +37.6% (-9.8% from Italy), Switzerland -7.1% (-2.9% from Italy), Australia -6.4% (-0.1% from Italy), South Korea -8.7% (-9.6% from Italy), Norway -4.8% (-7.8% from Italy), Brazil +11.9% (+12.9% from Italy), the Uk – data referring to January-November - -1.9% (+3% from Italy), Germany - from January to November - -9.7% (from Italy -10.1%), France -8.4% (from Italy -6.7%). In these 12 markets, overall imports are dropping by 0.8%, but mark +0.2% towards Italy. A result, which, for Italy, is led by sparkling sector, and, particularly, by Prosecco. Sparkling wines import (2024) towards Italy (while it is dropping almost everywhere at a world level) sees +11.2% from the Usa, +9.4% from Canada, +10.2% from Australia, +11% from China, +5.9% from Brazil, +3.8% from the Uk (from January to November), and +4.5% from France. Negative signs don’t miss, which, except for Norway, are lower of the general trend anyway: Japan (-6.3%), Switzerland (-7.3%), South Korea (-11.4%), Norway (-7.8%), and Germany (-9.6% from January to November). The total of imports in these 12 markets sees Italy at +4.8%, decisively better of -5.1%, of world data.

Sparkling wines, which, however, didn’t smile to France with -10.8% of volumes, a drop embracing all the main markets except for Brazil (+20.1%). As Denis Pantini added, “if in 2023, French wine export dropped due to the reduction of red wine sales out of the borders, in 2024, Champagne led downwards transalpine exports with 10% less of bottles shipped all over the world”.

Among the Italian PDOs, the leader is Prosecco (+12.3%) as value variation (2023/2024 compared to 2022/2023), but also white wines run: +8.2% for Veneto, +8.1% for Sicily, and +7.1% for South Tyrol, and Friuli-Venezia Giulia. Also red wines recover with +11.4% for Tuscany, +7.3% for Veneto, +3.6% for Piedmont, +3.3% for PDO sparkling wines. Down, on the contrary, Asti (-3.7%) and red wines from Sicily (-3.7%), but, which, however, improves compared to the previous year.

On the national market, explained Nomisma, the inflationary flame of the last years left a Italian consumer with lower expense capacity, and future expectations which are still characterized by caution. This is what emerges by sold wine quantities in Modern Distribution, which, in 2024, highlighted a reduction of almost -2% in Iper and Super channels, with higher peaks in the case of red wines (-4.6%), and sparkling wines (-7.4%). However, sold volumes held in discount registering also a value growth of 1.2%, particularly thanks to sparkling wines.

In this so complex and uncertain scenario, mined by revivals of protectionism, and threats of additional duties, the research of new end markets becomes increasingly more priority for the businesses of Italian wine. In these last three years, wine export from Italy grew in the areas of Eastern Europe, and Latin America: Poland (+26% compared to 2022), Czech Republic (+47%), Romania (+22%), Mexico (+3%), and Ecuador (+56%) are only some of the markets where Italian wines are increasingly more appreciated. Without forgetting Brazil, a great market of over 200 million of inhabitants, and part of the agreement of free trade between Eu and Mercosur, where red wines, particularly Tuscan and Piedmontese ones, are the most appreciated by Brazilian consumer, especially in South-eastern region with degree and medium-high income belonging to the generation of Millennials” as one can deduce by the deepening by Fabio Benassi, Project Manager Nomisma Wine Monitor. Wines, in Mercosur (2024), are growing in various aspects, from the production which arrived to 13.6 million of hectoliters (+9.7%), equal to 6% of the world one, to imports (+6%) touching 1.8 million of hectoliters (2% on a global scale). Consumption, in 2023, stopped at 11.8 million of hectoliters, an other growing trend (5% of the world consumption). Imports from Italy, in 2024, generated a value for 42 million euros (+12.3%), even if it is far from Chile (204 million euros), and Argentina (112 million) with Portugal (75 million), and France (57 million) preceding Italy, which “tears off” an average price per liter of 3.76 euros, higher than Chile, Argentina, and Portugal, but lower than France (8.62 euros). Share market in value of Italian wine in Mercosur is 8%.

A delicate topic emerged by the presentation is represented by consumers, and, particularly, by their evolution in light of the fact that, in Italy, in the main markets such as the Usa, most consumption is supported by over 60. “In Italy - declared Ilaria Cisbani, Market analyst Nomisma Wine Monitor – young people belonging to Gen Z consume wine only in special occasions, have a scarce knowledge of the product, and when they choose it, they pay attention to alcohol content and sustainability primarily. And, the same happens in the Usa, and this explains why “No-alcohol wines”, in the Usa, are already a widespread reality in the consumption of young generations”.

Among the speeches occurred during the day, it is important to signal that of Paolo De Castro, president of the scientific Committee Nomisma, former Euro Mp, and among the maximum experts of agriculture, who highlighted good news coming from Europe showing himself confident in a change of course which could give breathe and value to wine dealing with attacks of various types: “the Commissioner of Agriculture Christophe Hansen announced during the audition in the Agriculture Commission at the European Parliament that there will be a specific provision about wine. Regulations, which, probably, would translate into legislative act the work of Wine High Level Group which was an important step forward. The Commissioner confirmed that on February, 19th, there will be the presentation of the document of vision, which still circulates at an informal level, and I think that we can say that this change of course is present”.

About market evolution, particularly for red wines which are suffering more than sparkling wines, Carlo De Biasi, dg Agricola San Felice (Allianz Group) participated: “I always see the glass half full. My observatory is limited, we produce Chianti Classico, Brunello di Montalcino, and Bolgheri, denominations with a great history behind, and with consolidated and mature markets. The Usa and Italy are stable markets, the phenomenon of premiumization continued also in 2024 compensating the slight consumption drop, and gave positive results also in Canada, and in the Uk. There are markets which seem to be emerging, but with non continuous accomplishments, for example South Korea, where, in 2024, there has been an important slowdown, even if it seems to be recovering. Japan, Norway, and Sweden are dropping. From my observatory, I say that mature markets have variations, but remain the guiding light on which it is necessary to invest. The positive note comes from the Uk marking positive results in terms of positioning of the denominations, and in the last two-three years, the average price increased well, and mainly for Chianti Classico, it has been a surprise. Italy is important, for us, it is worth a third of sales, and it changed: today, the expansion concerns all the regions, it is not based primarily on Tuscany, and its tourism anymore allowing us to increase the sales. But, wine consumption in our country has been dropping for years, the approach to alcohol of new generations, the sanctions of the Highway Code, the aging of consumers, and the awaited demographic drop will bring us, probably, to a market which could be lower also than 20 million of hectoliters consumed in Italy. Be strong in our own homeland is the first point to be that way abroad. It is also up to us to be able to interpret our wines: climatic change imposed to review viticulture, we have to work in the winery to be identity, but also to meet a different consumption. Having an easier productive approach will allow us to cope with the market in a better way”.

Igor Boccardo, ceo Tenute Leone Alato-Genagricola, added that “home market is in difficulty with consumption. The modern channel is reacting with more promotions, more fliers, with a leverage on price which is not so much different from what happens in horeca, where a wine that a restaurant owner pays 6 euros is put on the wine list at a price of 30 euros. This unavoidably leads to a consumption drop. Export grows in a less strong and important way compared to the past, the competition is more complex, and there are significant realities on the market. The opening to new markets is certainly a positive thing also because there is an important desire of Italianness. An agreement such as that of Mercosur, which opens to new markets and simplifies the access, has positive consequences. Today, it is a very small market, the purchasing power in Mercosur area is not that of Germany or Switzerland, therefore, there will be also the theme of how to approach the market. There is really a lot to do, but they are only opportunities”.

On the contrary, regarding the theme of no-alcohol wines, the focus by Massimo Romani, ceo Argea, a group among the most important in Italy, concentrated on it: “today, compared to a year ago, a little way has been made. We have confirmations that, in addition to the interest, there is also the desire to purchase them. As Argea, we launched an anthology of 8 references covering a little all our brands, from red wines to white wines, up to sparkling wines, and, I have to say that we had the first commercial results. I went on a tour of suppliers in the Usa, and no one, except for Texas, said that they are not interested in this type of product, there is no state where we didn’t do a listing. This means that the market, despite being very small, exits, there is a listing of chains, and retailers for these types of products which begin to be present also in the horeca where they are served both in bottle, and more often “by the glass” for specific consumption occasions. There are requests also of more “smart” formats and containers, for example 375 cl ones. How much will it last? I believe that it will continue in time, the only answer I don’t feel to give is how big can this phenomenon become. But, there have been the first purchases, the signal is encouraging. We have to improve quality, but the last products launched on the markets are not bad. The possibility to experiment at home will allow us to improve. For new generations, it is necessary to find different communication modalities, but there are many wine producers that are already doing that. And, who managed to create a brand can take advantage of the ability to use it to talk about past in a little bit more creative way”.

Copyright © 2000/2026

Contatti: info@winenews.it

Seguici anche su Twitter: @WineNewsIt

Seguici anche su Facebook: @winenewsit

Questo articolo è tratto dall'archivio di WineNews - Tutti i diritti riservati - Copyright © 2000/2026

")

")

")

")

")

2026")

")

")

")

- La Selvanella 2025 (300x250)")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")