Sunday 26th of July 2026 - Last Update: 15:02

")

A turning point which speaks the language of wine and agrifood, reshaping the strategic weight of made in Italy starting from figures which mark a clear break: in the three-year period 2023-2025, public investment in the sector grows by +46% to 16.8 billion euros, alongside a structural base of 38.5 billion euros, putting an end to more than a decade of stability. Within this framework, the wine sector emerges as one of the most strategic and high-performing segments of the entire system, confirming its role as a pillar of the transition thanks to its global leadership in production and its central role in exports: in 2025, exports are worth 7.8 billion euros, corresponding to 11% of national agrifood exports, while globally Italy also consolidates its position as the world second-largest exporter (22.7% in 2024). The wine supply chain also benefits significantly from the support policies put in place, particularly the Supply Chain Contracts financed through the Nrrp and managed by the Ministry of Agriculture, which have mobilized a total of 7.8 billion euros in public and private resources: 1.4 billion euros is allocated to the wine sector, placing it among the main beneficiaries alongside the livestock and fruit and vegetable sectors (2.7 billion and 2.1 billion euros respectively). Its deep connection with the country cultural and territorial heritage, also recognized internationally, further strengthens the strategic value of wine: among the Unesco Intangible Cultural Heritage Sites related to agrifood, there are the traditional practice of bush-trained vine cultivation in Pantelleria and the Mediterranean Diet. These elements make Italy the only country in the world to boast six Unesco recognitions in the agrifood sector, surpassing Japan and Turkey. This is highlighted by the first Observatory on Agrifood Policies launched by The European House - Ambrosetti and Teha Group at the Forum Food & Beverage, held recently in Bormio, in Valtellina. The Observatory identifies 7 lines of intervention, including support for production chains, with 6.1 billion euros aimed at strengthening industrial capacity; investments in technological innovation and energy autonomy amounting to 5.6 billion euros for a digital and sustainable transition; support for consumption with 3.6 billion euros to protect purchasing power; food safety measures with 1.1 billion euros to address health and phytosanitary risks; and initiatives dedicated to young entrepreneurs (0.4 billion euros to encourage generational turnover), along with the promotion of made in Italy and the safeguarding of European balances.

All of this takes place within an integrated framework which, according to the proprietary methodology developed by the Observatory, generates a direct impact of approximately 87 billion euros in added value for the sector and an overall benefit for the national economic system estimated at 246 billion euros in the medium to long term. Of this, 67.8 billion euros is already visible over the next three years, while 178 billion euros is linked to structural effects on skilled employment, incomes, consumption, and competitive positioning in international markets. In this context, the supply chain employs a total of 3.4 million workers in 2024, including 485,000 in the Food & Beverage sector and about 2.9 million in the primary sector, with employment growing by +5.9% over the period 2015-2024. The agricultural sector, in particular, shows a leadership position at the European level in non-family employment, with about 948,000 workers and a share equal to 12.8% of the EU total, alongside growth of +2.9% compared to 2015.

At the same time, the total number of companies has decreased to around 1.1 million (-12.9% compared to 2015). Against a backdrop of increasing revenue and added value, this trend reflects a significant process of efficiency gains and strengthened productivity across the system. Moreover, when considering the extended supply chain, which includes intermediation, distribution, and catering, the economic value of the sector becomes even more significant: total turnover reaches 736.3 billion euros in 2024 (+39.1% compared to 2015) and, together with upstream and downstream supply chains, generates 400.4 billion euros in added value, contributing 20.4% to the national Gross Domestic Product (Gdp).

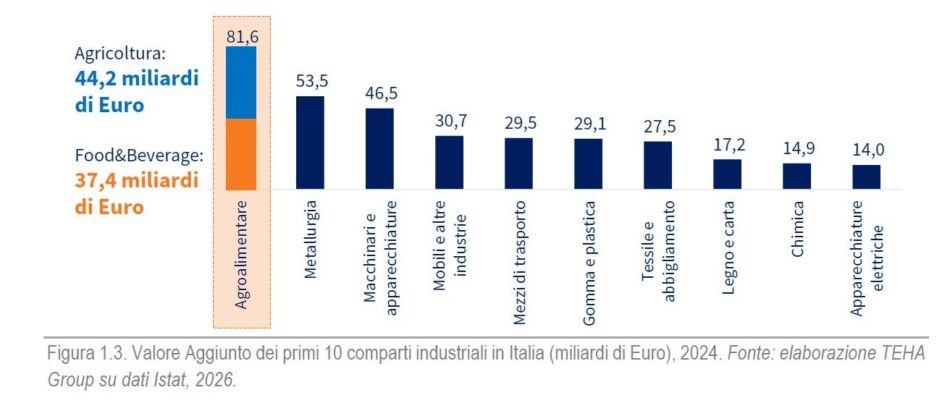

Evidence that fits into a context in which the agrifood supply chain confirms itself as the main driver of made in Italy, with a turnover of 269.9 billion euros in 2024, of which 193.3 billion euros generated by the Food & Beverage industry and 76.6 billion euros by the agricultural sector, +42% compared to 2015, and an added value of 81.6 billion euros as a direct contribution to Gross Domestic Product (Gdp), increasing by +42.4% compared to 2015, as highlighted by the Forum research “La Roadmap del futuro per il Food & Beverage: quali evoluzioni e quali sfide per i prossimi anni” - “The Roadmap for the future of Food & Beverage: what developments and challenges for the coming years”, which ranks the sector first among Italian manufacturing industries, with a value +50% higher than metallurgy, almost triple that of made in Italy fashion and about 5 times that of the chemical industry.

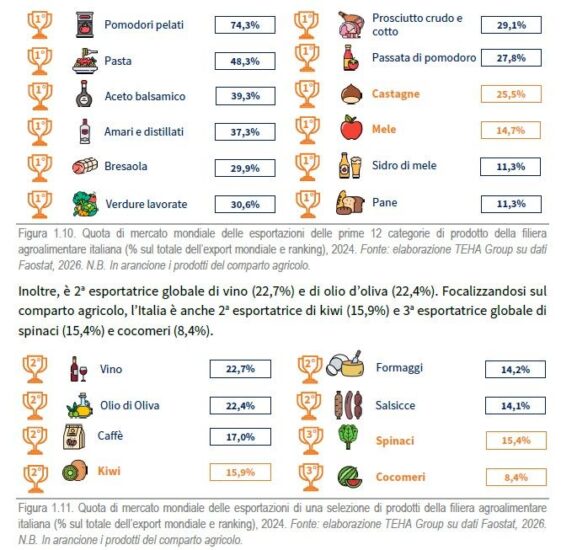

On the international front, 2025 marks highly significant results: agrifood exports reach record levels between 70.9 and 72.5 billion euros (including food & beverage, agriculture, and tobacco), almost doubled since 2015 (+96.4%) and up +5% compared to 2024, driven in particular by the Food & Beverage sector (62.5 billion euros including tobacco). Italy also ranks first among European competitors in terms of average agrifood export value, with 260.9 euros per 100 kilograms exported. This positive trend is observed despite complex conditions, including the introduction of tariffs in the United States which, at rates of 15%, led to a -4.5% decline in agrifood exports to that market in 2025.

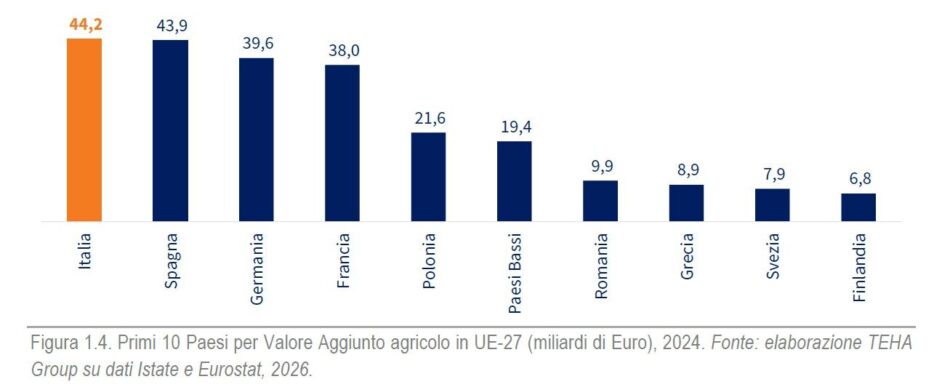

Confirming the system strength, the country consolidates its European leadership in agricultural added value, reaching 44.2 billion euros (+11% compared to 2023), and in the number of certified products: Italy ranks first in the EU for PDO/PGI certifications, with a total of 897 designations and a turnover of 20.7 billion euros. In this context, the wine sector emerges as one of the central and most profitable pillars of Italian agrifood: it accounts for 63% of total denominations (566 certifications) and a production value of 11 billion (+0.1% compared to 2023), exceeding that of cheese (5.9 billion euros) and meat products (2.2 billion euros). Globally, Italy also confirms its position as the second-largest wine exporter by market share, with 20.7% of total trade in 2024.

At the same time, territorial excellence models emerge, such as those of Lombardy and Valtellina. Lombardy stands out as Italy leading region for agrifood turnover (50 billion euros, +40.4% compared to 2015) and added value (11.2 billion euros, +31.6%), while the Province of Sondrio represents a notable example of integration between agriculture and tourism: it ranks fifth in Lombardy for wine production, with around 3.1 million bottles per year and a turnover of 22.3 billion euros. Valtellina is also home to the largest terraced vineyard system in Italy, with 850 hectares of vineyards and about 2,500 kilometers of dry-stone walls, an exceptional landscape and cultural heritage. “In this context, Lombardy and particularly Valtellina represent an excellence of the entire country system: the leading region in Italy for agrifood turnover, with 50 billion euros and growth of 40.4% since 2015 - affirms Valerio De Molli, managing partner and ceo of The European House - Ambrosetti and Teha Group - and also first in added value within the sector, with a contribution of 11.2 billion euros and growth of +31.6% since 2015. Lombardy is also Italy’s top region for agrifood exports, which have doubled in 10 years to 11.7 billion euros. Valtellina is a territorial model where identity, certified quality, production capacity, and openness to international markets come together, strengthening the competitiveness of Lombardy and of made in Italy agrifood”, concludes De Molli.

However, some structural challenges persist, including a strong dependence on pesticides and fertilizers. The report highlights that, in the case of a total cessation of their use, wine grapes would be among the most vulnerable crops, with an estimated production loss of 81%, similar to industrial tomatoes and just behind maize (87%) and rice (84%). At the same time, the agrifood sector contribution to national Gdp reaches a twenty-year record of 4.2% and, together with global leadership in iconic productions such as pasta, wine, and tomato products, strengthens Italy international positioning. This visibility was further amplified by the Milan-Cortina 2026 Winter Olympics, which acted as a reputational multiplier: during the weeks of the Games, digital reach volumes linked to the association “Italy and food” increased by 1.8 times compared to 2025. Analysis of global social media conversations shows that, alongside pizza and pasta, Italian wine (in its red, white, and premium variants) is one of the dominant keywords, with a positive or neutral sentiment of 87%.

In this scenario, and in the face of limited resources - just 0.7% of the world’s population and 0.06% of the global land area - Italian agri-food sector is proving to be an increasingly central system in the country economy and international projection. It is now called upon to turn the strengthening of investments into a stable and lasting competitive advantage.

Copyright © 2000/2026

Contatti: info@winenews.it

Seguici anche su Twitter: @WineNewsIt

Seguici anche su Facebook: @winenewsit

Questo articolo è tratto dall'archivio di WineNews - Tutti i diritti riservati - Copyright © 2000/2026

still in history")

")

")

")

")

")

")

2026")

")

")

")

- La Selvanella 2025 (300x250)")

")

")

")

")

")

2026 (300x120)")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")