Tuesday 28th of July 2026 - Last Update: 19:10

")

Antinori, Frescobaldi and Santa Margherita in terms of profitability, Cantine Riunite-Giv (Gruppo Italiano Vini), Caviro and Botter at the top in terms of turnover: these are the top players in Italian wine, after a very tough 2020 for the entire sector, as emerges from the report on the wine sector signed by Mediobanca, Sace and Ipsos.

A ranking that reflects, in terms of numbers and changes in turnover, a very hard year in which, in general, the realities more focused on out of home and high-end have suffered more, while those already well present in large-scale distribution and with the core business on a more popular product range, and strongly export-oriented, have gained market share.

If we look at the fundamental parameter of profitability, that is, the ratio between net profit and turnover, the absolute leader is Antinori (26%), ahead of Frescobaldi (24.5%) and Santa Margherita (24.2%), that is, three of the most articulated wine producers with the best market positioning. The leader for percentage of growth, instead, is the Italiana Wine Brand group (+29%), in front of Contri Spumanti (+13.8%), Caviro and Mondodelvino (both +10%), Cavit (+9.6%), La Marca (+8.7%), to close with Botter (+6.4%) and Schenk Italia (+5.7%).

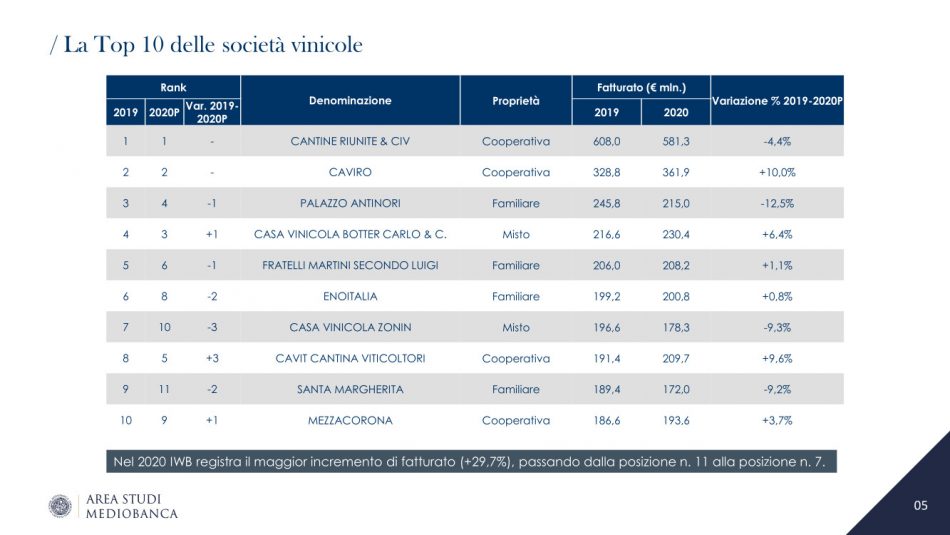

The leadership of turnover in 2020, on the other hand, is confirmed to be the prerogative of the Cantine Riunite-Giv group, with turnover at 581 million euros (-4.4% compared to 2019), clearly distanced from the second position held by another cooperative, the Romagna-based Caviro, whose turnover, on the other hand, grew by 10%, approaching 362 million euros. On the podium, the Veneto-based Casa Vinicola Botter (230 million, +6.4%, and acquired in recent months by the Clessidra Fund, ed).

Above “quota 200”, by turnover, are confirmed Antinori, with 215 million euros (-12.5%), Cavit, leader of the Trentino cooperation (2020 turnover equal to 210 million euros, +9.6% on 2019), and again the Piedmontese Fratelli Martini (208 million euros, +1.1% on 2019), Italian Wine Brand (204 million, +29.7%) and the Venetian Enoitalia (201 million euros). And then, above 100 million euros, there are in order, Mezzacorona (193.6 million euros, +3.7%), Zonin (178.3, -9.3%), Santa Margherita (172, -9.2%), La Marca (152.9 +8.7%), Terre Cevico (127.3, -3.9%), Mondodelvino (122, +10%), Cantina di Soave (120, 8, -11.2%), Schenk Italia (117.5, +5.7%), Contri Spumanti (107.1, +13.8%), Ruffino (106.3, -19.4%), Frescobaldi (106, 12.9%), Collis Veneto Wine Group (104.8, -3.8%), Vivo Cantine (101.1 -6%) and the wine division of Gruppo Campari (100.4, -9.2%).

A ranking that, in all likelihood, next year will be decidedly different, at least in terms of turnover, not only due to the effects of what everyone hopes will be a full recovery, but also due to the effect of the process of mergers and acquisitions seen in recent months, such as the operation Italian Wine Brands - Enoitalia, which has created a group with a potential turnover of over 400 million euros, or those of Fondo Clessidra, which has brought together under its ownership the control of Botter and Mondo del Vino, for a turnover estimated at 352 million euros.

Copyright © 2000/2026

Contatti: info@winenews.it

Seguici anche su Twitter: @WineNewsIt

Seguici anche su Facebook: @winenewsit

Questo articolo è tratto dall'archivio di WineNews - Tutti i diritti riservati - Copyright © 2000/2026

still in history")

: Boscarelli, one of Vino Nobile tops, invests in future")

")

")

")

")

")

")

")

2026")

")

")

")

- La Selvanella 2025 (300x250)")

")

")

")

")

")

2026 (300x120)")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

in 2026 Top 20 performers")