Friday 10th of April 2026 - Last Update: 18:39

")

")

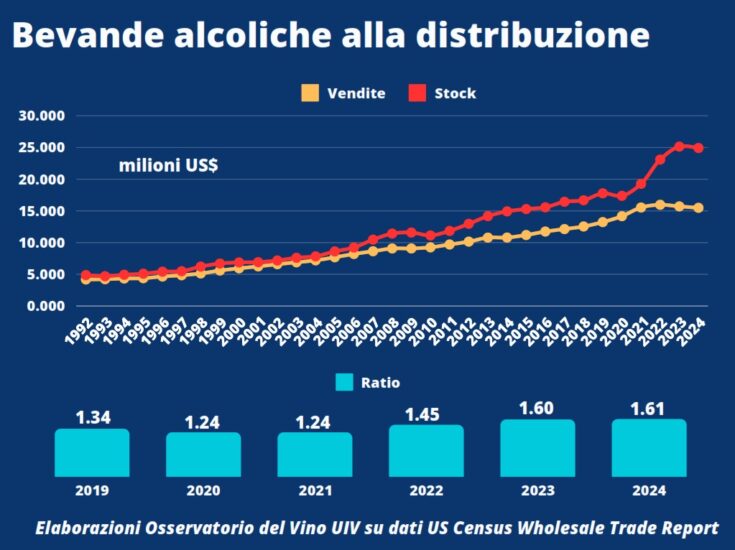

From Italian wineries, wine to the U.S. is leaving, as Istat data on the first 3 months of 2024 speak of a +2.2% in value for Italian exports to the States. But overall consumption, in the most important American market, continues to decline. Despite the breath of fresh air in April (+2%), the trend balance of the first 5 months based on warehouse orders from horeca and large retailers marks -8% in overall sales and -6% for products from Italy, which suffers, but does better than competitors such as France, the USA itself, Australia and Spain. And even the hypothesized end of the inventory surplus among retailers remains a pipe dream, as the ratio of alcohol stocks to actual sales still travels at very high levels with a surplus of about $10 billion. This is according to an analysis by the Uiv-Vinitaly Observatory based on SipSource, a platform that measures sales - and actual consumption in the short term - in 75% of U.S. retail establishments. The Observatory’s U.S. Focus reports a general decline by all major supplier countries with the exception of Chile (+12%), which has been betting heavily on balance prices. Italy (-6%) does better than France and the United States (-8%), Australia and Spain (-11% and -10%), but not the hitherto stainless New Zealand, which also fell into negative ground (-1%).

For our country, the negative signs are scattered with full force: from Pinot Grigio (-7%) to Chianti (-14%), with the news that doing less worse this time are the reds (sub-zero since September 2022), which close the 5 months at -6.5% against -8% for whites. It could have been worse, according to the Uiv-Vinitaly Observatory, without the stability of Prosecco (-0.6%) and Asti (+1.6%), but especially without the significant growth of non-Prosecco Charmat Methods (+7%), which are now worth 24% of the volumes of Italian sparkling wine consumed in the US. A figure in sharp contrast, that of low-cost Italian Charmats (average consumer price around $13), with respect to the trend of bubbles in the world’s top market, with Champagne at -15%, Spanish Cava at -11% and domestic sparklings at -11%. A figure, finally, evidently generated by the strong cocktail trend that increasingly embraces the category, with tumultuous growths between $8 and $13: +40% from January to May.

A bottom-up drive that seems for now to be concentrated in two well-defined areas: the West Coast (+36% sales and 30% share) and the Midwest (+9% and 18% share).

“We knew it would be a complicated start to the year”, said UIV president Lamberto Frescobaldi, “but we also know that Italian wine has adequate antibodies to react to difficulties. At this stage, however, we need to make the right moves: there is a need to sustain a change that has been taking place for 20 years in the Italian vineyard. The sector is adapting to changing consumption styles by modifying its production potential better than other countries, proof of which is that today Italian sparkling wines represent 33% of the Italian total wine consumption in the U.S., almost four times more than the general sparkling share (9%). Now we need to do more, starting from promotion to business policies-from managerialism to flexibility-that must be embraced by institutions, without giving in to welfarist chimeras that are highly detrimental to development”.

The current general picture - the analysis concludes - also seems to cast doubt on certainties that have hitherto been taken for granted, such as premiumization. Aside from a few prestigious names (Brunello di Montalcino and Chianti Classico, but also superior Bordeaux, Pomerol and Margaux, Uiv points out) that generally mark growth, among the Old Continent’s classics, the luxury segment (above $50 per consumer) seems to be losing its luster, with Italian reds at -8% and French ones even at -16%. Difficulties also for ultra-premium whites, between $25 and $50: the total market is at -10%, with Italy at -12% France at -6% and New Zealand at -18%.

Copyright © 2000/2026

Contatti: info@winenews.it

Seguici anche su Twitter: @WineNewsIt

Seguici anche su Facebook: @winenewsit

Questo articolo è tratto dall'archivio di WineNews - Tutti i diritti riservati - Copyright © 2000/2026

, sparkling wines protagonists for 52%")

")

")

")

2026")

")

")

")

- La Selvanella 2025 (300x250)")

")

")

")

")

")

2026 (300x120)")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

will distribute Champagne Encry in Italy")