Sunday 21st of June 2026 - Last Update: 20:24

")

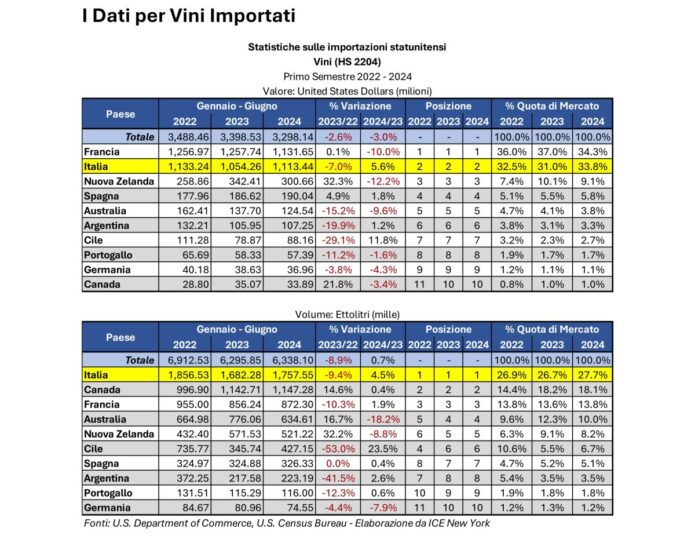

The wine market, even in the U.S., is not shining, there is no shortage of economic difficulties, and there is great uncertainty ahead of the presidential election, now just around the corner. But overall, things are not so bad for Italian wine, which remains the absolute leader among imported wines in the world's most important market, and which is growing more than average, at least in the first 6 months 2024. This was stated in a note from Ice in New York, headed by Erica Di Giovancarlo, on market trends between January and June 2024, analyzed by WineNews. The data say that the U.S., in the first half of the year, imported 6.3 million hectoliters of wine, 0.7% more than the same period 2023, for a value, however, at -3%, for $3.3 billion. Well, in this picture, Italy exported 1.8 million hectoliters of wine, up +4.5%, remaining the leader in volume, ahead of Canada, which exported 1.1 million hectoliters of wine to the U.S. (+0.4%), but almost all of it bulk wine (which, however, accounts for just 3.4% of Italian wine exports to the U.S.), and France, at 872. 300 hectoliters, at +1.9%, while Australia (643,600 hectoliters, -18.2%), and New Zealand (with 521,200 hectoliters, at -8.8%) lose sharply ground. But things seem to be going well in value, too, for Italy, which grossed $1.11 billion, at +5.6% over the first half of 2023, significantly better than the market and even its first competitor, France, now caught up, at $1.13 billion, down -10%. With Italy, therefore, holding a 27.7 %share in volume and 33.8% in value among important wines in the US. A result, Ice in New York points out, also achieved thanks to the fact that “Italian wines continue to offer consumers exceptional value for money and the diversity of its regions, styles and varieties offers numerous options to American consumers thirsty for new experiences”.

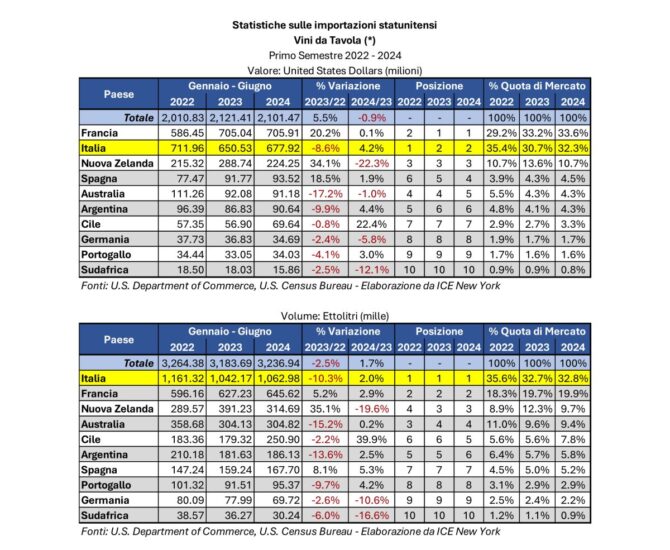

And in fact, looking at the different types of wine, Italian wine does better than the market average in all categories, from whites, which are the most imported type to the U.S. from Italy, to sparkling wines, which almost equalize still whites in quantity and value, to reds, which although the smallest category, in quantity, continue to be the most profitable in value. In fact, Ice explains, white wine was the subcategory with the highest import volume in the first half of 2024, continuing the trend of previous years. America imported 1.6 million hectoliters of white wine, or 49.6% of all its table wine imports, despite a -2.1% in volume and -4.2% in value, for $958 million.

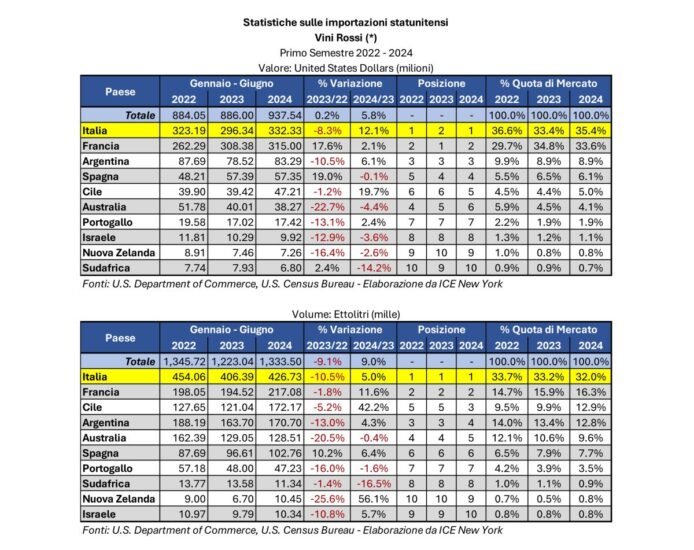

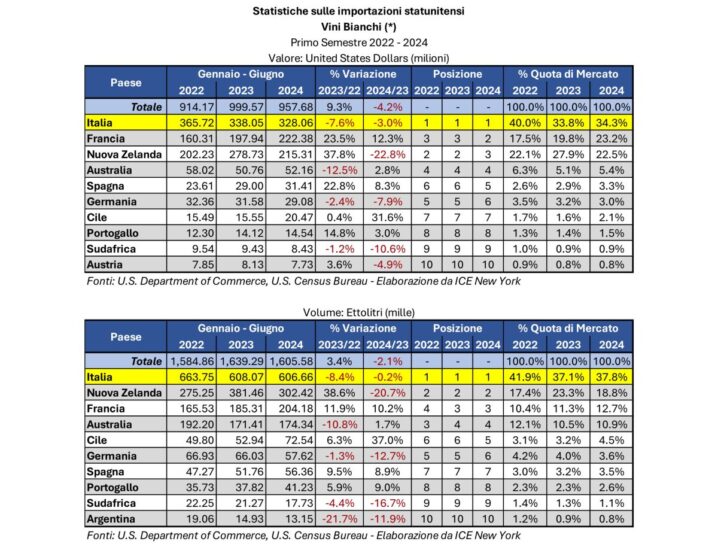

In this context, Italian white wine held the largest market share in both volume (37.8%) and value (34.3%). Having done better than the category, Italian exports fell -0.2% in volume to 606,000 hectoliters, and -3% in value to $323 million. With growing interest, operators report, in wines with good acidity, light, and varieties such as Vermentino, Falanghina, Grillo and Verdicchio. Looking at reds, however, in the first 6 months 2024 the U.S. imported 1.3 million hectoliters of red wine, accounting for 41.2% of U.S. table wine imports, at +9% in volume and +5.8% in value, to $937.5 million. Italy, on red wines, was the top country in both volume and value, with 427,000 hectoliters (+5%) for $332 million (+12.1%), with the trade highlighting the good momentum of wines from varieties such as Barbera, Nero d’Avola and Sangiovese.

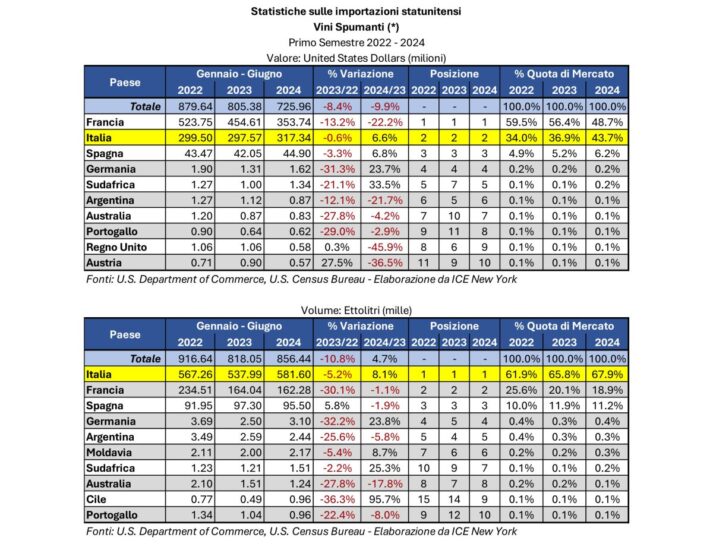

Looking at the sparkling wine chapter, however, the U.S. imported a total of 856,000 hectoliters (+4.7%) for $726 million (-9.9%) in the first 6 months of 2024. Even in the case of bubbles, Italy did much better than the market average, with 583,000 hectoliters (well over half of the total, at +8.1% in volume) for $317 million (+6.6%). “Industry professionals”, explains Ice in New York, “have noted that Prosecco in particular remains popular with American consumers. Compared to the other two most popular European sparkling wines, French Champagne and Spanish Cava, Prosecco continues to benefit from a strong price/quality ratio, remaining at a more affordable price point than luxury Champagne, while exhibiting a perception of higher quality and greater brand recognition than the more competitively priced Cava. In contrast, U.S. consumers could benefit greatly from greater awareness of the wide range of sparkling wines made in Italy. In the United States, “Champagne” is often used interchangeably with “vino spumante”, and consumers generally tend to see any Italian sparkling wine as “Prosecco”. Investments are needed by stakeholders throughout the distribution chain, from producers to consortia to importers, to increase brand awareness of other Italian sparkling wines, e.g., Franciacorta and Trentodoc. A point of confidence in the category is on-premise sales, where U.S. consumers prefer imported sparkling wine in a 2:1 ratio to American sparkling wines. Amid declining wine sales among middle-income consumers, affluent consumers continue to purchase premium sparkling wines in restaurants”.

Completing the panorama, Ice further explains, are rosé wines, which, however, are in sharp decline, in general, in the U.S., and for Italy represent a small slice, with 28,000 hectoliters for $17 million in the first half of the year, in a segment, however, in which France dominates with more than 80% in volume and slightly less in value, and with Italy being second in market share, but below 10% in both parameters, but also dessert or fortified wines, whose imports to the U.S. are increasing in volume (277,000 hectoliters, +21.1%), but down in value ($299 million, -3.7%), with Italy also growing in this segment, with 53,600 hectoliters (+9.2%) for $105 million (+11%).

All this, explains Ice, which processed data from the U.S. Department of Commerce, in a framework in which if the overall interchange of the U.S. with the rest of the world recorded a growth of +2.9%, that with Italy, as a whole, marks +11.4%, and with the food and beverage sector making +19.7%. In a market, the U.S., remains the most important in the world for wine, a product that seems stable in consumer preferences. Today, in fact, if you look at the world of alcoholic beverages, spirits in 2023 accounted for 42.2% of sales, ahead of beer, with 41.8%, which, however, is losing ground, while wine stopped at 16.1 %, in value. And while beer has steadily lost market share to spirits since 2000, Ice further points out, wine has remained consistently between 15% and 17%, with sales amounting to about $300 billion.

Contributing to the rise of spirits are changing demographics and consumer interests. The new generation of consumers seeking alcoholic beverages seeks the “experiential” aspect of customized cocktails and non-alcoholic drinks in restaurants and bars and prioritizes the convenience and diversity of ready-to-drink beverages when at home or in other “on-premise” social settings. This is a scenario in which even wine, while strong in its solidity in the preferences of Americans, must look carefully to envision its future.

Copyright © 2000/2026

Contatti: info@winenews.it

Seguici anche su Twitter: @WineNewsIt

Seguici anche su Facebook: @winenewsit

Questo articolo è tratto dall'archivio di WineNews - Tutti i diritti riservati - Copyright © 2000/2026

")

")

, but decrease under 50 million hectoliters")

, Piedmont (+0.5%), Tuscany (-8.3%) on the podium")

")

")

")

")

")

2026")

")

")

")

- La Selvanella 2025 (300x250)")

")

")

")

")

")

2026 (300x120)")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")