Friday 20th of March 2026 - Last Update: 16:16

")

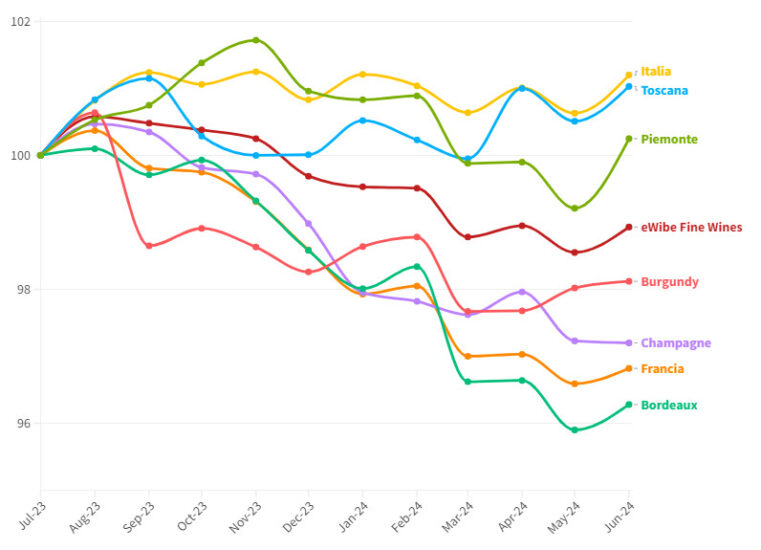

That the first half of 2024 has not been easy for great collectible or high-value wines either is a fact, as confirmed by the indexes of the British platform Liv-Ex, but also by the half-year balance sheet of a luxury giant with many top wine and Champagne brands, such as Lvhm. But the fine wine segment still shows some solidity. “The rebound in June - with Piedmont recording the best performance - however, was not enough to bring back the positive sign in the first six months of the year. The bottles that increased their value the most were Salon’s 2008 Cuvèe Le Mesnil (+29.5%), Tenuta San Leonardo’s 2013 San Leonardo (+26.8%), Gaja’s 2014 Gaia & Rey (+23.2%), Biondi-Santi’s 2004 Brunello di Montalcino Riserva Tenuta Greppo (+22.9%) and Tenuta di Trinoro’s 2018 Tenuta di Trinoro (+22.5%). While the bottles that found the most interest (views, clicks, and searches) were Tenuta San Guido’s Sassicaia 2021, Antinori’s Tignanello 2021, and Montevertine’s Le Pergole Torte 2021 (which are also among the top five best-selling wines along with Roerder’s Cristal 2015 and Bollinger’s Rd 2008), and again Ferrari Trento’s Giulio Ferrari Riserva del Fondatore 2010 and Château Lafite Rothschild’s Château Lafite Rothschild 2020. While the highest value lot transacted was a 3-bottle case of Clos de la Roche Grand Cru 2011 from Domaine Leroy, at 27,000 euros”. This is stated by the Observatory of the specialized platform eWibe, a live market for fine wines, which includes all the major investment labels from the most representative countries in the sector, and marks a -0.6% decline in the first half of 2024. France (-1.1% since the beginning of the year) is still suffering, especially in the wake of Bordeaux’s disappointing “En Primeur” campaign, with the 2023 vintage seeing an average price cut of about 30%, as we have often reported on WineNews. Italy (-0.1%) once again shows a path of stability.

Looking at the individual regions, Tuscany continues to maintain its positive trend, registering +1% in the twelve months, while in the first six months 2024 its growth stands at +0.5. As also anticipated in previous versions of the Observatory curated by eWibe analysts, the conviction remains that Tuscan wines will be the absolute protagonists of the coming months, especially due to the still very low pricing compared to the great French vintages. Piedmont, eWibe further explains, registers a more moderate growth of +0.3% over the twelve months, while it confirms some stability over the six months, marking the best performance in June (+1 percent), compared to +0.5% in Tuscany. Increased demand is reported on vintages released earlier, 2016 and 2019 in the lead, while we remain waiting to assess market trends in 2024 for the releases of Barolo 2020 and Barbaresco 2021.

French regions, on the other hand, continue to record disappointing numbers compared to Italy: Bordeaux does -1.8% since the beginning of the year, Champagne -0.8%, Burgundy -0.5%. Despite this, June marks positive growth for all French regional indices. “France, after experiencing a major downturn in 2023, now offers attractive investment opportunities, particularly in the Bordeaux region for vintages already on the market. Demand for Champagne remains high but, in sharp contrast to the scarcity of the past two years, volume supply has returned to standard levels. Reflecting this, the increase is smaller month-on-month. The region is seeing the release of fine vintages in the last period with Krug 2011 leading the way and the latest vintage from France’s most emblazoned Maison, Dom Pérignon 2015, which eWibe launched, among the first in Italy”. As for Burgundy, eWibe notes a tentative return to normal after a period of readjustment, which led to a widespread decline in the past year. There is cautious optimism regarding the 2022 vintage, characterized by a very good quality of the harvest, especially on the reds.

“The data and performance give breath to the whole sector and reflect the excellent releases so far presented by the main producers”, says Leonardo Bernasconi DipWsey, Head of Wine eWibe, “and France, after experiencing a major downturn in 2023, now offers interesting investment opportunities, particularly in the Bordeaux and Champagne regions. The price drop that occurred for some labels and vintages represents, today, an attractive buying opportunity. The disappointing "En Primeur" campaign in Bordeaux, leads to increased demand on the secondary market for already available vintages. In fact, some of the most prized bottles from previous vintages are in some cases positioned at the same price levels, when not lower, than the 2023 “En Primeur” releases, despite the fact that the average score and quality of the vintage are higher”.

Copyright © 2000/2026

Contatti: info@winenews.it

Seguici anche su Twitter: @WineNewsIt

Seguici anche su Facebook: @winenewsit

Questo articolo è tratto dall'archivio di WineNews - Tutti i diritti riservati - Copyright © 2000/2026

")

")

")

")

")

")

")

2026")

")

")

")

- La Selvanella 2025 (300x250)")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")