Saturday 5th of July 2025 - Last Update: 18:29

")

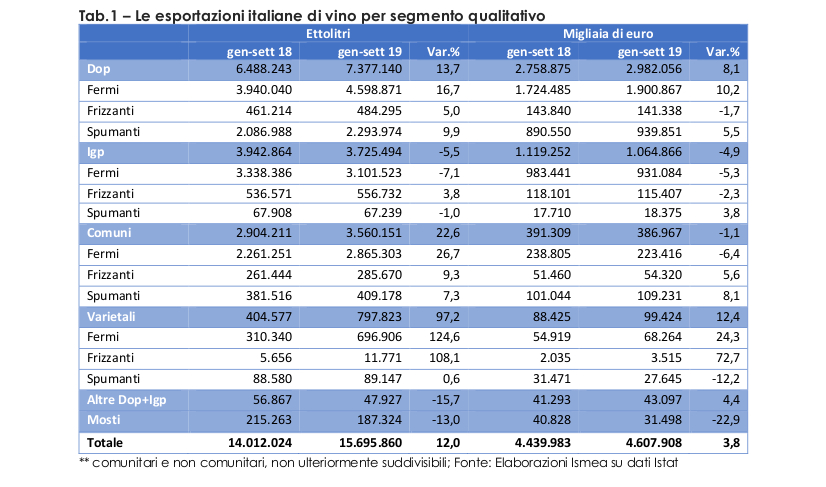

In the first 9 months of 2019, as already reported by WineNews on Istat data, Italy exported wine for 4.6 billion euros, with a growth of almost +4% over the same period of 2018 (for a volume of 15.7 million hectoliters, at +12%). And a decidedly interesting aspect, highlighted by Ismea's analysis, is that during the period, exports in value to third countries amounted to 2.32 billion Euros, compared to 2.29 billion Euros to the EU. If the end-of-year data confirm this difference, Ismea points out, there will be an overtaking ever recorded from the beginning of the new millennium to the present. An overtaking due to a growth in value more than double in Third Countries compared to the EU (+5% vs. +2%), while in volume it is the European Union that has grown significantly more than non-EU markets (+15% vs. +6%).

Overall, points out Ismea, if the trend of the last few months of the year is maintained, at the end of the year there could be over 22 million hectolitres for a record value of 6.5 billion euros, but with slower growth than expected a few years ago, with average prices falling both for dynamics linked to wine lists and for the different mix that makes up the export basket. In fact, the most important increase was in ordinary wines which, with 3.6 million hectolitres, mostly in bulk, grew by 22% in volume, accompanied, however, by a slight drop in revenue, as a result of the sharp reduction in production price lists, which in the last year, 2018/2019, reached 27%.

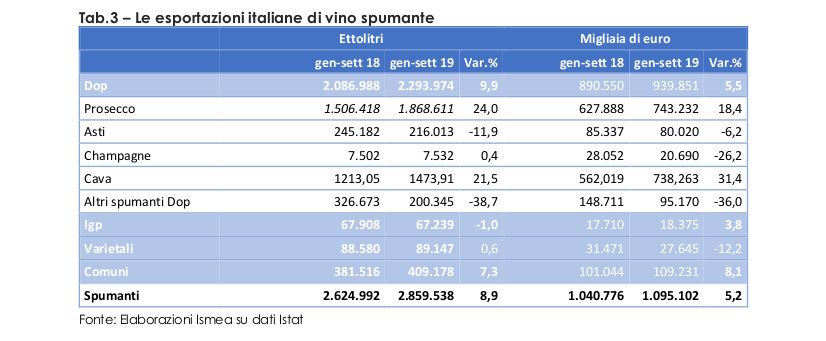

The growth of sparkling wines continues (+9% in volume and +5% in value) but now without the double-digit increase we were used to. Also in this case we must consider Prosecco, whose sales abroad are increasing both in volume (+24%) and in value (+18%), while Asti, for example, shows important difficulties in maintaining market share.

There was also a marked increase in PDO wines, especially still wines, which offset the reduction recorded in the PGI segment.

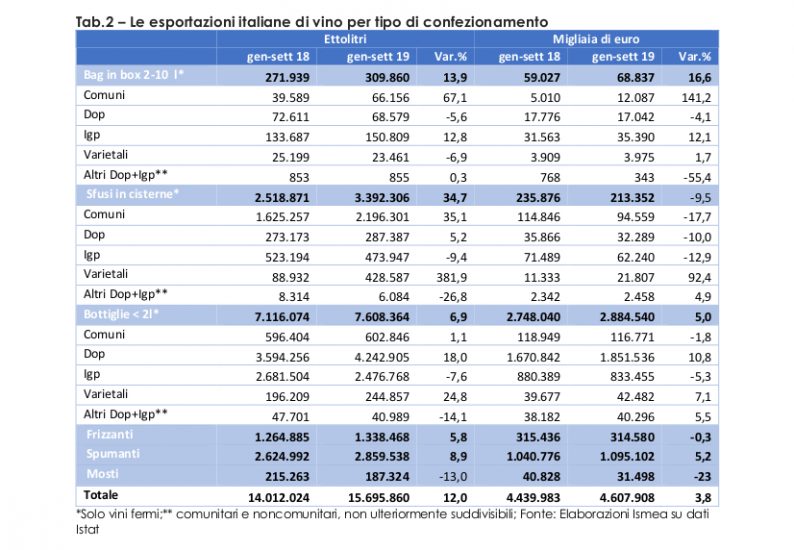

This “transfer” is due, at least in large part, to the consolidation on the market of Pinot Grigio Delle Venezie PDO. PGIs, however, showed a decisive setback both in still wines in the bottle (-8% in volume and -5% in value) and in bulk (-9% in volume and -13% in value), while they performed particularly well in bag in box (+13% in volume and +12% in value).

In the first nine months of 2019, however, this type of packaging grew significantly compared to the same period of the previous year, while foreign demand for sparkling wines appeared to be growing but not as dynamic as for other segments. Looking at the list of customer countries, it seems appropriate to underline that, although Italian wine now reaches a large number of destinations, the first three destinations absorb more than half of the total exported both in volume and value.

In terms of customers, the recovery in volume achieved especially in the summer of exports to the United States is noteworthy. The increase in quantities recorded in the bottled PDO segment (+11%) more than offset the significant drop in PDI (-24%). Sparkling wines also performed well, with an increase in the first nine months of the year of 11% in volume and 10% in value. It is also important to underline in the US market the double-track trend between Prosecco, which grew at a rate of 40% over the same period of 2018, and the rest of Italian sparkling wines, which instead lost ground. On the US market, there is expectation and concern about the increase in duties, which, although they are not affecting Italian wine at the moment, are still keeping the attention high. Exports to Germany have increased sharply, where Italian exports grew by 24%, driven by +47% of bulk wines, which, with over 2 million hectolitres, represent 46% of the total imported from Italy, offset, for the reasons mentioned above, by a very limited increase in revenue (+3%).

The German market is bucking the trend compared to Italian sparkling wines, with demand down 9% in volume due to a drastic reduction in demand for both ordinary sparkling wines and Asti, while Prosecco continues its progression, achieving an 11% increase in quantity for a 4% increase in turnover.

Another market that deserves particular attention is that of the United Kingdom, where the first nine months of 2019 marked an increase in quantities for Italian wine, while the price of the same was at a standstill. With the exception, in fact, of bottled still wines for all other segments there was a drop in average values. On the negative side of the trade balance of the wine sector, the first nine months of 2019 showed a marked reduction in Italian demand also because the availability of the 2018 harvest was particularly abundant.

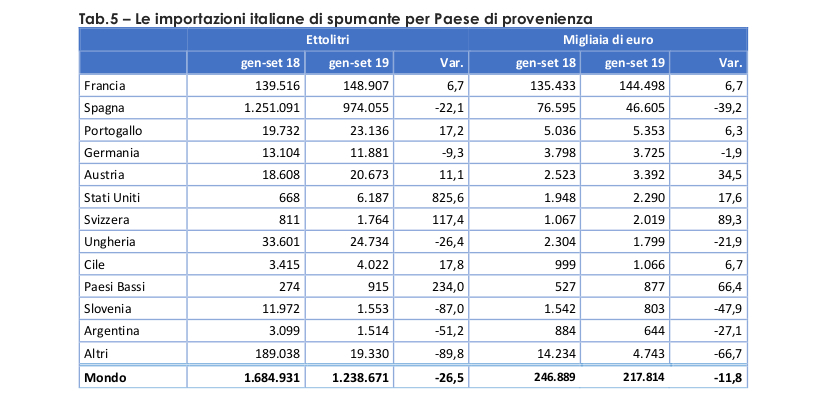

Purchases outside the national borders were reduced by a quarter compared to the same period in 2018 thanks to the blending of bulk wine requests (-31%) which, with 918,000 hectolitres, represent 74% of the Italian import basket. There was also a clear reduction in the import of sparkling wines. The first to have undergone such a blending of Italian demand, primarily on bulk but also on bubbles, was Spain. On the other hand, imports from France increased both for bottled wines and sparkling wine.

Copyright © 2000/2025

Contatti: info@winenews.it

Seguici anche su Twitter: @WineNewsIt

Seguici anche su Facebook: @winenewsit

Questo articolo è tratto dall'archivio di WineNews - Tutti i diritti riservati - Copyright © 2000/2025

")

2025")

- La Selvanella 2025 (300x250)")

")

")

")

")

")

")

")

")

")

")

Sito")

")

")

")

")

")

")

.gif")

")

")

")

")

")

")