Sunday 21st of June 2026 - Last Update: 20:24

")

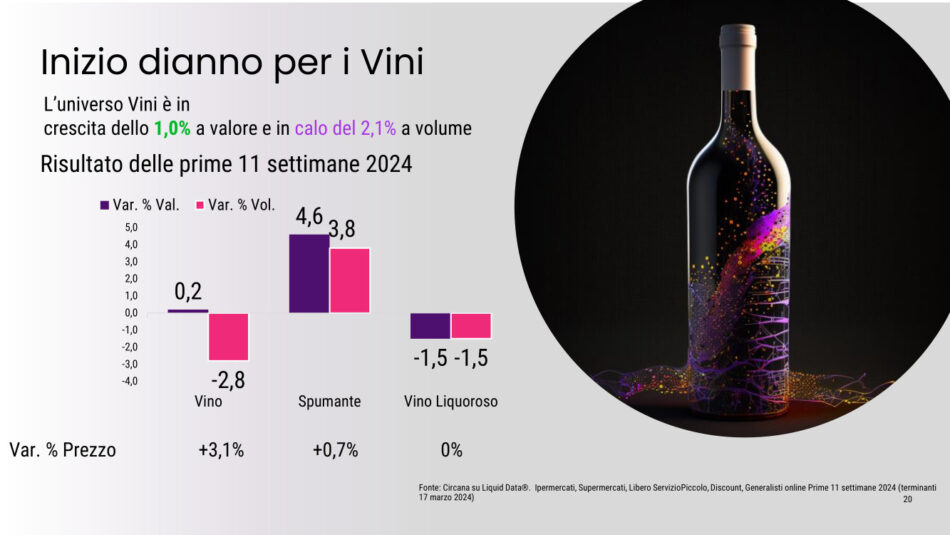

The large-scale retail trade remains, unquestionably, a solid channel for wine sales, thanks to an increasingly sought-after variety and with the effect of promotions that incentivize consumers to complete a purchase. But understanding how wine sales are doing in large-scale distribution also means taking the pulse of the situation, taking a snapshot of the health of consumption and how much the inflation effect affecting households affects volumes. In addition, of course, to observing the changing preference landscape, with the growth of whites and bubbles climbing the “approval ratings”. Data for the first quarter of 2024, meanwhile, report slightly better volume sales than the close of the year 2023 even though the scenario remains complicated. 0.75-liter bottles of wine drop in volume by 2.2% over the same period in the previous year, but the full-year 2023 figure saw a larger drop of 3.2%. Decidedly better are sparkling wines, which return to the positive (driven by Prosecco) with +3.8% over the same period of the previous year, while in the full year 2023 they lost 1.1%. This is reported by the Circana study for Vinitaly presented at Vinitaly 2024 during the round table on wine and large-scale distribution organized by Veronafiere, and anticipated in recent days.

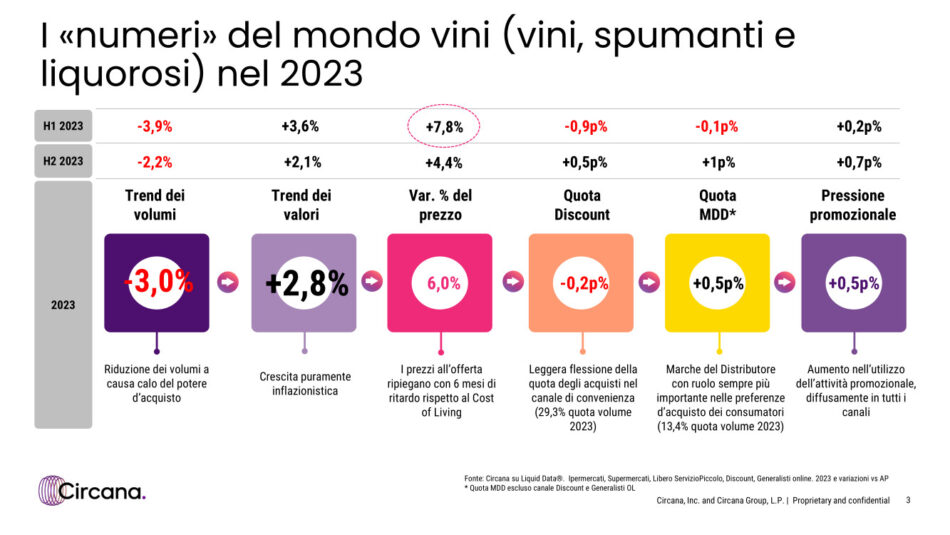

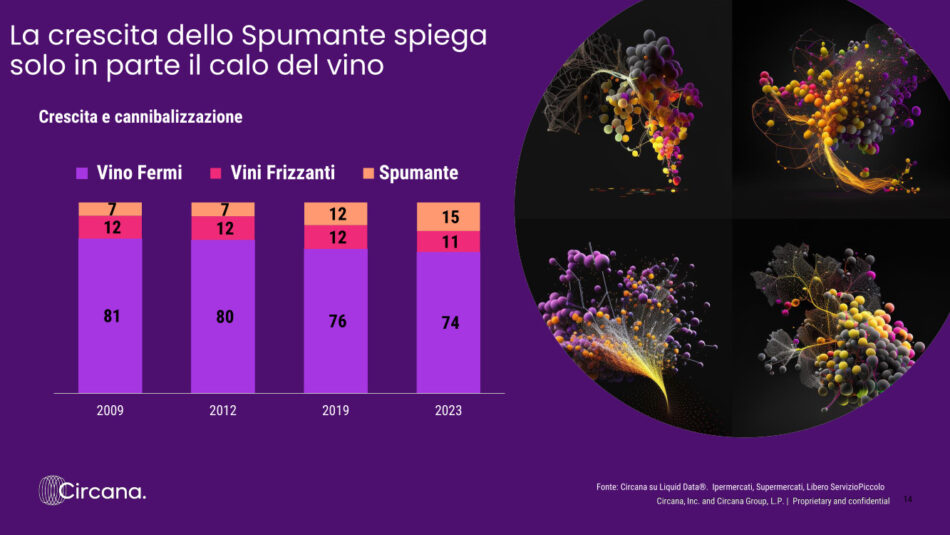

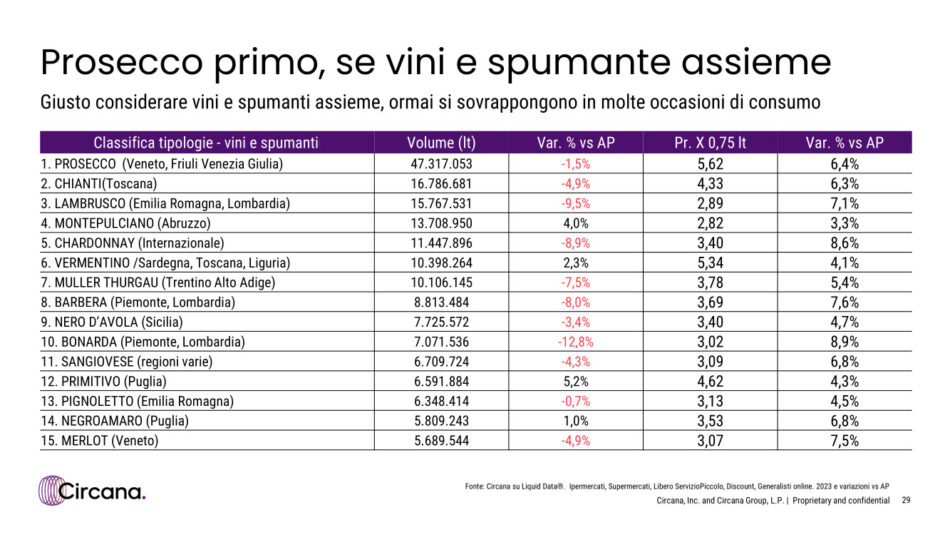

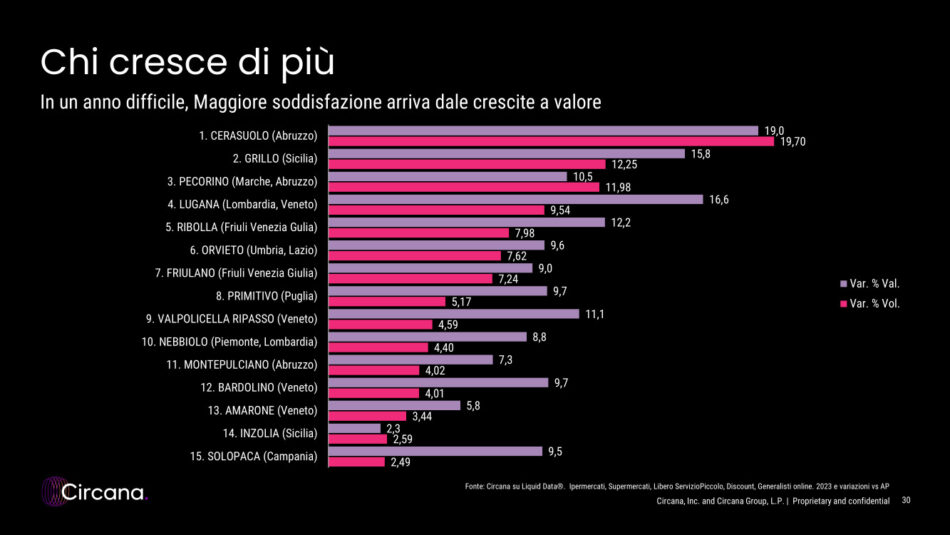

It seems, therefore, to confirm a trend that, after a strongly negative second half of 2022 and first quarter 2023, saw sales gradually rise again in the second part of 2023. A trend that, together with data from the first quarter of 2024, could, perhaps, lead to a year of moderate recovery (data from the first quarter of 2024 take 11 weeks into consideration). What seems clear, however, is that in 2023, confirmation emerges that consumer tastes are changing: whites and bubblies are going faster than reds, a type that dropped last year by 3.9% while remaining the best-selling type with 276 million liters with white wine, on the other hand, stopping at 245 million liters (-1.6%) and thus losing less. A trend that has been evident for several years: the volume share of red wine has dropped from 54% in 2009 to 49% in 2023; white, on the other hand, has risen from 40% in 2009 to 45%. Rosé wine is also growing (Cerasuolo is first in the 2023 ranking of “emerging” wines) although it is a wine with a modest market share in large-scale distribution; still wine, with 33 million liters, is up 1.5% identical performance for sparkling rosé sparkling wine, with 6 million liters. The price of 0.75-liter bottles with designation of origin (Doc, Docg, Igt) rose by 6.3% per liter in 2023, while the price of sparkling wine increased by 5.9%; promotions increased by 0.5% (Circana for Vinitaly, 2023 data, Hypermarkets, Supermarkets, Small Free Service, Discount, Online Generalists).

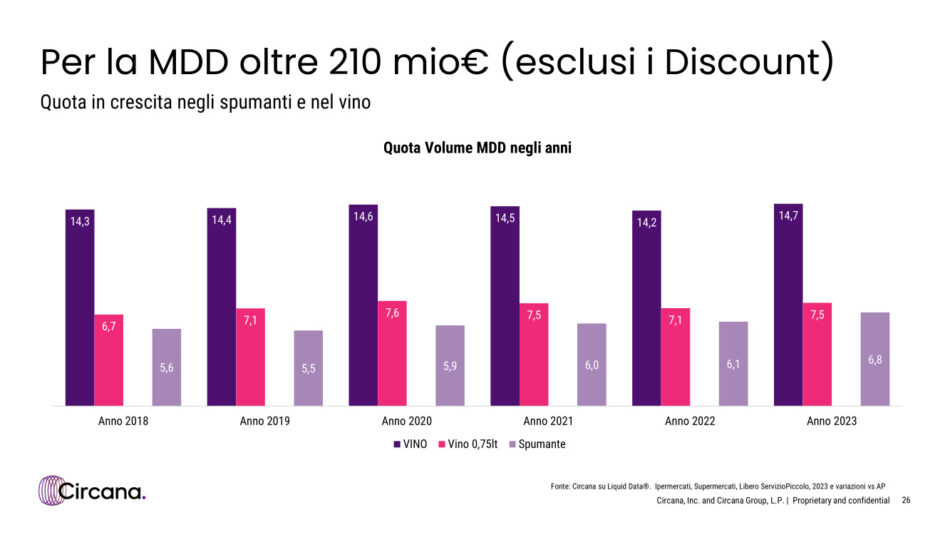

There are two scenarios for 2024. Should wineries and retail focus primarily on volume recovery, they should opt for controlled price increases and hard-hitting promotions. In a scenario, on the other hand, of more focus on defending margins, then it could come down to list price increases and the consequent realignment of selling prices, as well as prudent increases in promotional budgets. Circana for Vinitaly reported how sales of private label (Mdd) wines are increasing in real terms, experiencing a small drop in volume in 2023 of 0.6%, while Mdd sparkling wines grew by 1%. As for organic wines, wine fell 1.1% as opposed to sparkling wines (+11.8%).

“Wineries”, Virgilio Romano, Circana Business Insight Director, tells WineNews, “have to get used to it, facing this scenario, understanding that the pie cannot be expanded in terms of volume. But they must at least preserve it from the point of view of values: it is something they already do because in recent years the value of wine has increased, budgets and supply chain are safeguarded. But it is clear, though, that all this has to be transferred to the consumer, the increased value cannot be a higher price, it has to be something to be explained and justified otherwise the breathing space is short term and not long term”.

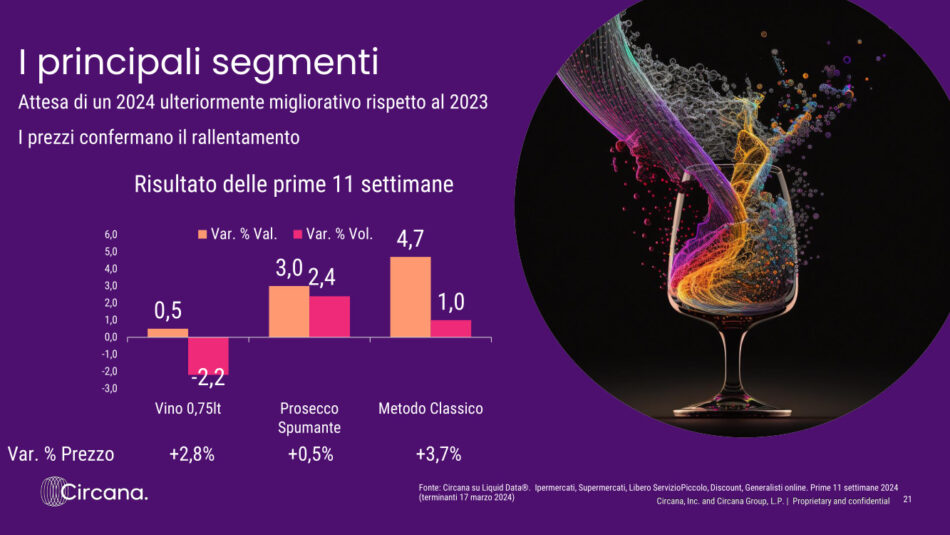

“For Coop, you have to work for a proper margin”, explained Francesco Scarcelli, Head of Beverage & Frozen Foods Coop Italy, “that is, a margin in promotions aligned with the shelf margin. Improving discounts to support promotions could be the common goal of production and distribution to try to safeguard volumes”. Scarcelli pointed out to WineNews that for wine, the three-point increase in value in 2023 is data influenced “mainly by inflation. As we noted, per capita consumption is declining. Mdd wines did better in the market in 2023, also closing with negative but slightly better numbers. In the first 11 weeks 2024 branded wine is at -2.8%, there is nothing to be particularly happy about, sparkling wines are saved a bit, which are trending slightly against the trend, however, red wines, especially, are suffering. Private labels have given a security of purchasing power protection to the end consumer on a daily basis. The moment this tension softens, however, private labels also begin to suffer a bit”.

For Mirko Baggio, Federvini representative, Villa Sandi large-scale retail sales manager, “using only promotional leverage is no longer enough, we also need to support shelf positioning with adequate communication that can enhance the brand and refer to territory and type of product involved”.

Communication and innovation to speak to new generations are the points to work on for Francesca Benini, Uiv-Unione Italiana Vini representative, Sales & Marketing Director Cantine Riunite & Civ: “young people consume less wine and are attracted by green attributes, product origin, low alcohol content. How can we, together with distribution, drive a change that is already underway?”.

Consumer changes that translate into “less structured drinking, fresher and easier to combine with lighter, quicker and healthier meals”, said Simone Pambianco, National Category Manager Conad, “they are also paying attention to the new regulatory information on the label, for example the energy value”.

Showing optimism Marco Usai, Wine Specialist Md, “we are looking forward to the year that has just begun, our first quarter closed positively in both volume and value, with a significant decrease in promotional pressure on 2023”.

Lorenzo Cafissi, Beverage & Home & Personal Care Director Carrefour Italia, also spoke about communication: “Large-scale distribution is trying, together with companies in the sector, to find new communication and business support levers to bring new life and regain volume, consensus and interest”.

There was also no shortage of references to non-alcoholic, or dealcoholic, wine, which is beginning to appear on the shelves of various retail brands, including Conad, Coop, Esselunga, Eurospin, and Lidl.

Copyright © 2000/2026

Contatti: info@winenews.it

Seguici anche su Twitter: @WineNewsIt

Seguici anche su Facebook: @winenewsit

Questo articolo è tratto dall'archivio di WineNews - Tutti i diritti riservati - Copyright © 2000/2026

")

")

, but decrease under 50 million hectoliters")

, Piedmont (+0.5%), Tuscany (-8.3%) on the podium")

")

")

")

")

")

2026")

")

")

")

- La Selvanella 2025 (300x250)")

")

")

")

")

")

2026 (300x120)")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")