Sunday 21st of June 2026 - Last Update: 20:24

")

sul 2019")

Even with the world in Pandemia, the vineyard has run its course and the producers, grappling with the difficulties linked to Covid but also with the challenges of all time, starting with the management of climate change, have now concluded the 2020 harvest everywhere. Which, according to the first OIV - International Organization of Vine and Wine, presented today in video-conference by General Manager Pau Roca, is substantially in line with 2019, with a production of must and juice of around 258 million hectoliters, +1% on last year. An estimate based on data from 30 countries representing 84% of the world’s wine production, which announce a production below the average of recent years, OIV underlines. This in itself is not a great evil, given the current market context, slowed down by Covid, but also by international tensions, duty wars and phenomena in the process of materializing such as Brexit.

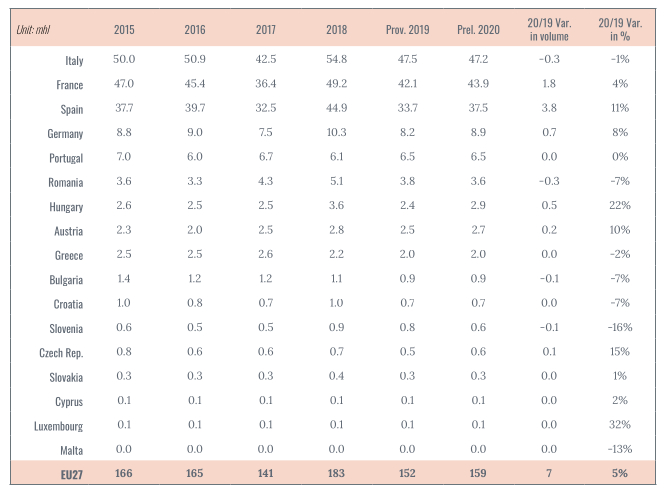

If this is the overall picture, however, the situation changes from zone to zone. In the European Union, for example, production is estimated at 159 million hectoliters (excluding juice and must), up 5% on 2019. A growth almost entirely attributable to +11% in Spain (on 37.5 million hectoliters) and +4% in France (43.9 million hectoliters), while Italy drops by -1%, but remains the largest producer country, with an estimated 47.2 million hectoliters. 3 Countries that, Oiv recalls, alone make 81% of the production of anthems in the European Union, and 49% worldwide. Among the other countries of the Union, still growing production in Germany (+8%, 8.9 million hectoliters), Hungary (+22%, to 2.9 million hectoliters) and Austria (+10%, to 2.7 million hectoliters), while Portugal is in line on 2019, at 6.5 million liters, and are declining Romania (-7%, to 3.6 million hectoliters) and Greece (-2%, to 2 million hectoliters). Substantially stable, despite the difficulties created by the fires in California, production in the U.S. is expected to be 24.7 million hectoliters, while no estimates are available for China.

More consolidated data, however, are those coming from the southern hemisphere, where the harvests closed in the first quarter of 2020. And here the loss is -8%, for a total of 49 million hectoliters. With production collapses in all major producing countries: -17% in Argentina (10.8 million hectoliters), -11% in Australia (10.6), -13% in Chile (-10.3), while production is growing in South Africa (+7%, 10.4 million hectoliters) and New Zealand (+11%, on 3.3 million hectoliters), and Brazil stable (2.2 million hectoliters).

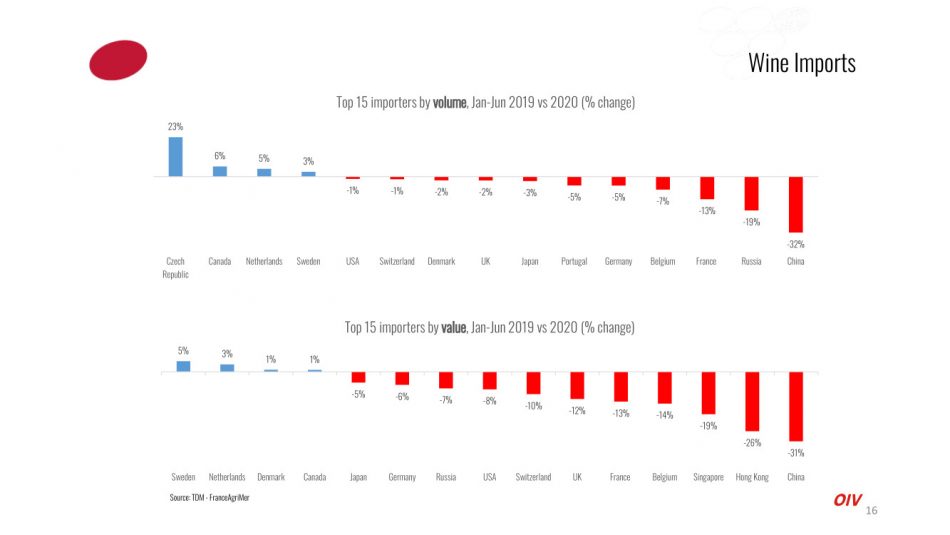

But, net of production, what is worrying, of course, is the market: according to OIV - International Organisation of Vine and Wine, according to estimates by France AgriMaire, in the first half of the year, between January and June 2020, wine exports fell in volume and value for most of the main exporting countries. Emblematically, -21% of France, while as more analysis confirms, Italy seems to have held up, with a -4%, as well as, for example, France and the U.S., which stopped the losses, in the first half of 2020, at -7% and -9%.

Among the major importers in value, weighs -31% in China (accompanied by -26% in Hong Kong and -19% in Singapore), but also -14% in Belgium, -13% in France, -12% in the UK, -10% in Switzerland, -8% in the USA, -7% in Russia, -6% in Germany and -5% in Japan. On the positive side, among the top importers, only 4 countries: Canada and Denmark (+1%), the Netherlands (+3%) and Sweden (+5%). Data that, however, in the year-end balance, except for miracles, seem to be largely destined to be even more negative.

“The 2020 production will enter a 2021 market still heavily conditioned by Covid - stressed the director of OIV / International Organization of Vine and Wine, Pau Roca - and the containment measures have already had a strong impact on the sector, in the most important markets are estimated drops in value sales between -15% / -20%, although the situation changes from country to country and will be decisive the last 3 months of the year. Some things will return to normal, other changes will remain, wineries will have to adapt. There will be great economic difficulties for the sector, and for this reason it is essential that governments recognize the wine production chain as strategic, and support it. But it is also true that the wine sector has always shown great ability to adapt to the difficulties, and will do so again. One of the most important keys will be digital evolution and the development of e-commerce, which has been accelerated by the pandemic, and will continue to grow impressively, according to analysis. We, like Oiv, are also implementing our “digital transformation”, which will also result in the creation of a constant Observatory on the market, and a “digital garage”, a sort of incubator of digital startups related to wine, as well as an integrated system of data analysis from multiple sources, to support the whole sector”.

And to the WineNews question on what the OIV/International Organisation of Vine and Wine can do to ensure that the governments of the world really consider viticulture an essential activity, Pau Roca answers: “For many of our countries viticulture is fundamental. The production of wine, and grapes, is an essential activity, like the rest of agriculture. We think that a large part of the world’s grape production is not transformed into wine, but becomes food. We try to transmit this idea to everyone, because we believe in it”.

Copyright © 2000/2026

Contatti: info@winenews.it

Seguici anche su Twitter: @WineNewsIt

Seguici anche su Facebook: @winenewsit

Questo articolo è tratto dall'archivio di WineNews - Tutti i diritti riservati - Copyright © 2000/2026

")

")

, but decrease under 50 million hectoliters")

, Piedmont (+0.5%), Tuscany (-8.3%) on the podium")

")

")

")

")

")

2026")

")

")

")

- La Selvanella 2025 (300x250)")

")

")

")

")

")

2026 (300x120)")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")