Thursday 23rd of July 2026 - Last Update: 10:21

")

Two pillars of the Italian economy, on an economic level, but with a strength capable of generating spillover, positive, on other sectors as well, from tourism to agriculture, and also capable of communicating Italian value and style in the world, another aspect of fundamental importance. These are the Italian wine and restaurant sectors, both symbols of made in Italy, but which spent a 2023 with a different “sentiment”.

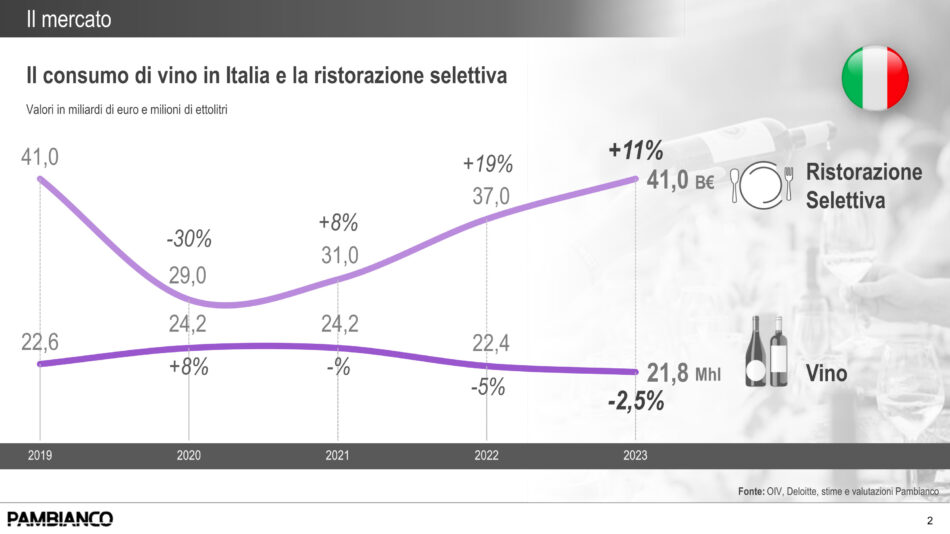

It was certainly not a memorable year for wine, struggling with a slowing market and declining production due to climatic reasons, but also consumption that is curbed, both due to prices and a health trend “driven” by young people (products with lower alcohol contents and alcohol free are on the rise) and a greater polarization between high quality and cheaper wine choices. On the other hand, there is the so-called “selective” catering, which continues its growth after the “dark years” of Covid, and where new formats are being born in a market that is still very fragmented, however, and where the process of concentration (chains) continues with the need for capital for development. And while there is always more internationalization of the format, there is no shortage of opportunities in fine dining for Italian formats internationally. And then there is commercial catering that appears to be healthy and where the Italian “top 10” are all growing in 2023. Elements highlighted by edition No. 4 of Pambianco’s “Wine & Food Summit”, organized in partnership with PwC, which offered a series of insights into strategies and new trends in the global market for the sector.

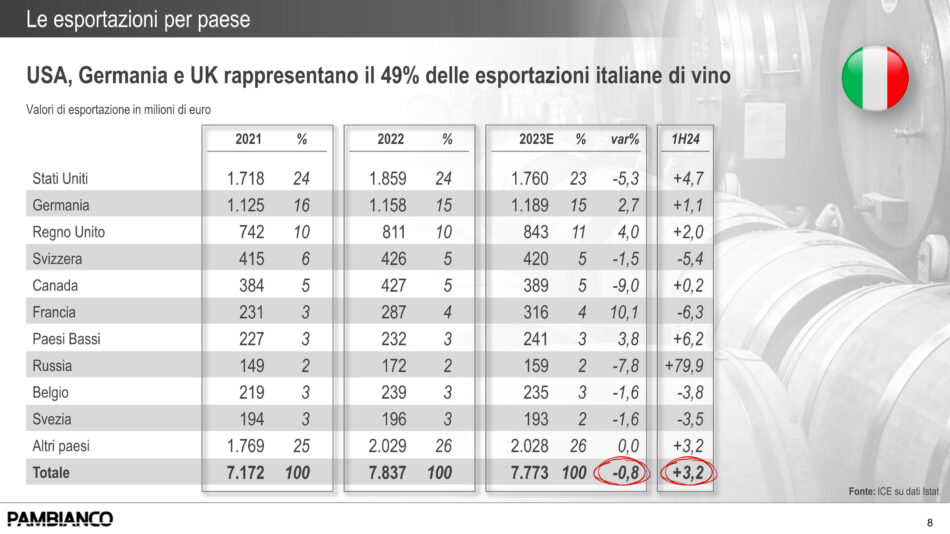

With a production value of 38.3 million hectoliters of which 21.4 are exports and a total domestic consumption of 21.8 million hectoliters, the Italian wine market, in 2023 fell to second place in the production ranking by volume (16% of total production) behind France (20%). With domestic consumption of 21.8 million hectoliters in 2023, down -2.5% on 2022, it is exports that give more satisfaction to the sector, registering a smaller drop (-1%) thanks also to the increase in average price. First markets for Italian exports were confirmed to be the U.S., with 23% of the total, but down 5.3%; Germany, worth 15% of exports and growing 2.7%; and the U.K., which now weighs 11% and rises 4%. The first half of 2024, however, marks a recovery in exports to the United States (+4.7% over the same period 2023). At the global level, looking, finally, at the ranking by consumption in millions of hectoliters, Italy is on the lowest step of the podium with 21.8 million hectoliters consumed (10% of the world total), behind the United States (15%) and France (11%).

Still, looking at the market leaders, the top 10 Italian companies in the wine-commercial segment, Pambianco reports, turnover 3.3 billion euros, up both on 2022 (+2%) and, to a greater extent, on 2021, when they slightly exceeded 3 billion. Leading the “top ten” is the Italian wine cooperation giant, Cantine Riunite & Civ (of which Gruppo Italiano Vini - Giv is part, ed.), with 674 million euros, ahead of Argea (438 million euros, +3%), Iwb (429 million euros, -0.3%), Caviro (419 million euros, +3%), Cavit (267 million euros, +1%), La Marca Vini e Spumanti (226 million euros, -4%), Fratelli Martini Secondo Luigi (218 million euros, -8%), Mezzacorona (218 million euros, +2%), Collis (209 million euros, +65%), and Zonin1821 (195 million euros, -3%).

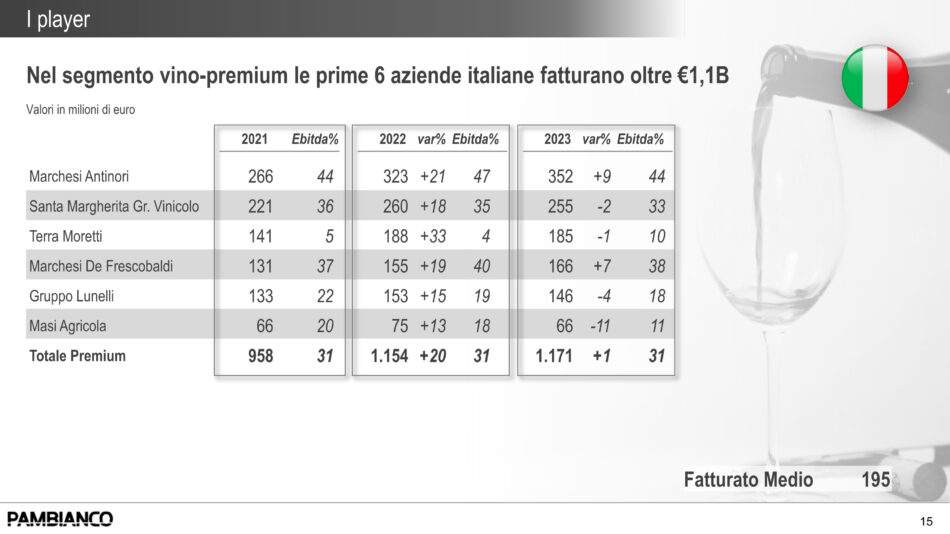

In the wine-premium segment, according to Pambianco’s classification, on the other hand, the top six Italian companies, in 2023, exceeded, as revenues, 1.1 billion euros (+1%) with an Ebitda index, and thus gross operating margin, at 31, on average, compared to 8 for the “top ten” in the commercial wine segment. Leading the “top” is the family par excellence of Italian wine, Marchesi Antinori, with 352 million euros (+9%), ahead of Santa Margherita Gruppo Vinicolo of the Marzotto family (255 million euros, -2%), and closing the podium is Terra Moretti (185 million euros, -1%), another large family business in Italian wine, as well as Marchesi Frescobaldi (€166 million, +7%), the Lunelli Group, the symbol of Italian bubbles in the world (€146 million, -4%), and Masi Agricola, among the symbols, however, of Valpolicella Classica and Amarone (€66 million, -11%).

Regarding online and wine e-commerce in particular, Pambianco again highlights, after the boom in the Covid period, we are witnessing a phenomenon of “normalization,” but still capable of producing important numbers: it leads Tannico with 64 million euros in 2023 over 2022 (-6%), which precedes Bernabei, protagonist of an excellent result (28 million euros, +24%), and Vino.com (27 million euros, -22%). The online total of the top 5 players is 143 million euros (-7% over 2022).

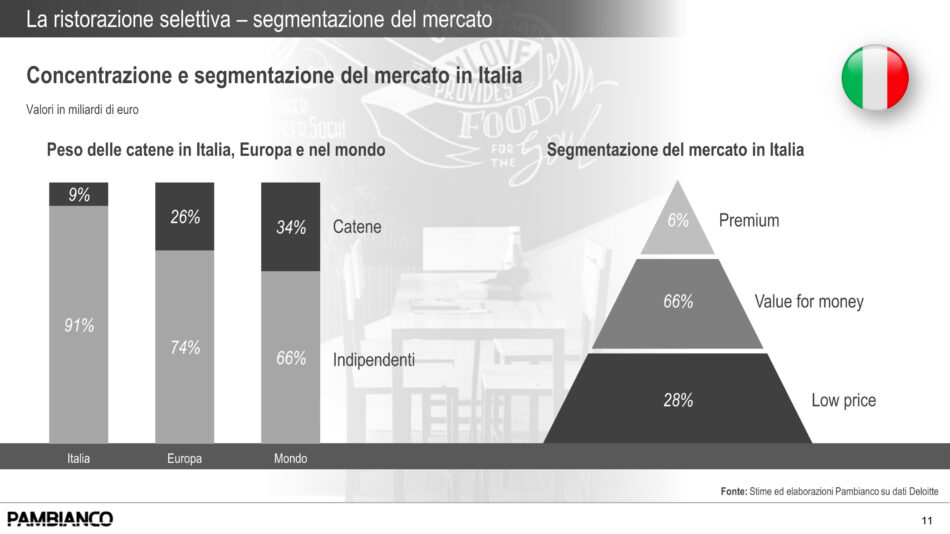

In terms of what Pambianco calls selective catering, however, the global market is worth more than 1.2 billion euros in 2023. Italy takes 3% of the global total, and is fifth in the world and first in Europe. The Italian market still appears very fragmented with chains accounting for 9%, compared to a European average of 26% and a world average of 34%. In terms of starred restaurants, there are 380 in the Belpaese (+1% over 2022), ranking third after France (635) and Japan (387).

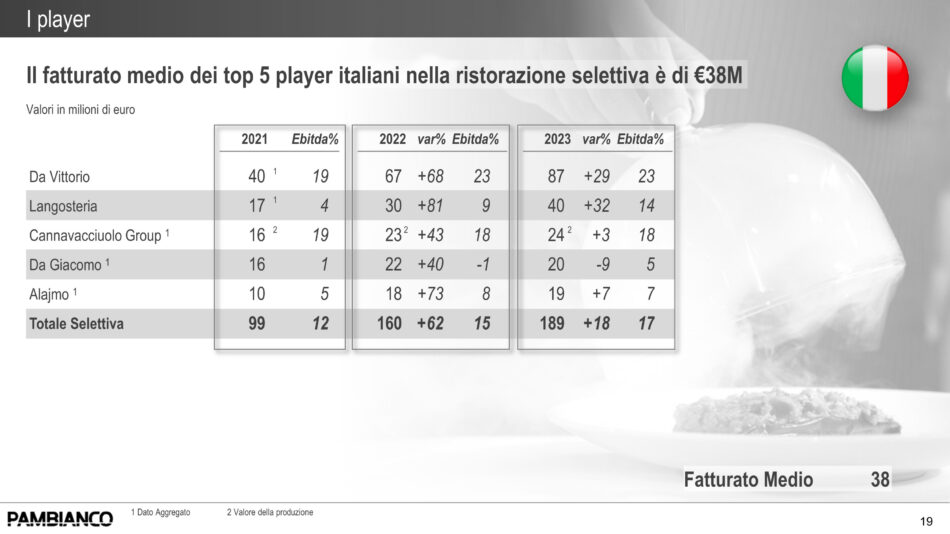

The average size of selective catering companies is, however, still small with the top five billing, in aggregate, 189 million euros in 2023, up 18%, but profitability is attractive with an average of 17%. Leading the way in sales is Da Vittorio, owned by the Cerea family, with 87 million euros (+29%), ahead of Langosteria (40 million euros, +32%), Cannavacciuolo Group (24 million euros, +3%), Da Giacomo (20 million euros, -9%), and Alajmo (19 million euros, +7%). In contrast, the average turnover of the top 10 Italian players in commercial catering was 1.7 billion euros in 2023, up 18% over 2022. Leading the ranking is Chef Express with 425 million euros (+24%), which is ahead of Cigierre (Old Wild West, Pizzikotto) at 417 million euros (+8%), RoadHouse Spa (220 million euros, +15%), La Piadineria (193 million euros, +39%), and My Chef Ristorazione (164 million euros, +15%).

Still, at the investment level, PwC Italy points out, the food sector, is considered a “defensive” segment, and therefore attractive to private equity funds either for direct investment or through companies already in their portfolio. The niches of greatest interest are frozen food, ingredients, nutraceuticals, pet food, and foods aimed at meeting specific nutritional characteristics (e.g., foods for celiac disease sufferers). There have already been major investments on these categories in the past by private equity funds, which may now consider monetizing or targeting aggregations with other players. The wine sector was also affected by major aggregation deals in 2020-2022, and 2025, according to analysts, “may be the good year for exit” by those who invested, to monetize.

Positive sentiment is also recorded about a selective restart of M&A in the restaurant sector, with a preference for seat-free fast dining models. With growing confidence, then, on increasingly informal dining models in line with today's lifestyles and changing consumption patterns.

Copyright © 2000/2026

Contatti: info@winenews.it

Seguici anche su Twitter: @WineNewsIt

Seguici anche su Facebook: @winenewsit

Questo articolo è tratto dall'archivio di WineNews - Tutti i diritti riservati - Copyright © 2000/2026

: Boscarelli, one of Vino Nobile tops, invests in future")

")

in 2026 Top 20 performers")

")

")

")

")

")

")

")

2026")

")

")

")

- La Selvanella 2025 (300x250)")

")

")

")

")

")

2026 (300x120)")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")