")

Tuesday 17th of March 2026 - Last Update: 18:14

")

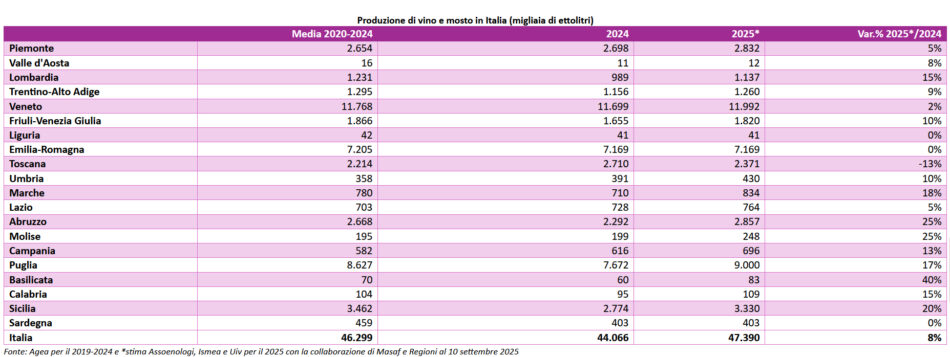

To 39.8 million hectoliters of wine in stock, registered at the end of July 2025, with the first grapes of the new harvest already picked, another 47.4 million hectoliters are expected to be added to them, the result of the 2025 campaign, which is underway across most regions and marked by healthy grapes and without particular issues. This points to a very good or excellent vintage in nearly all areas with peaks of excellence. These estimates come from Assoenologi, Unione Italiana Vini - Uiv, and Ismea, presented today in Rome at the Ministry of Agriculture. Based on current data, therefore - keeping in mind that conditions in the vineyard can change quickly - the 2025 production should register an increase by 8% compared to 2024, bringing volumes back in line with the average of recent years after two particularly poor vintages (+2% compared to the 2024–2025 average). A harvest that confirms Italy’s global leadership in wine production volume, a record that is less desirable in a time when the wine market is undergoing a slow but structural contraction. Italy is followed by France (37.4 million hectoliters, with just released downward revisions) and Spain (forecasted at 36.8 million hectoliters).

Considering regional classification, with nearly 12 million hectoliters, accounting for a quarter of the national harvest, Veneto confirms Italy’s top wine-producing region, followed by Puglia and Emilia-Romagna at 19% and 15%, respectively. Together, these three regions make up 59% of Italy’s total production. Sicily and the Abruzzi follow in “the top five”, pushing Piedmont and Tuscany (which sees a double-digit drop of -13%) to sixth and seventh place in the list. The expected production increase is uneven across the country. The South drives the growth (+19%), encouraged by Puglia’s strong performance (+17%). Northern Italy also sees growth, though more modest, with the Northwest (+8%), including a notable rebound in Lombardy (+15% compared to last year, though still -8% below the 2020–2024 average). The Northeast is also up (+3%), despite a variable summer and a rainy spring which required careful disease management. Friuli-Venezia Giulia leads the increase (+10%), followed by South Tyrol (+9%) and Veneto (+2%), which shows limited growth after a 2024 harvest in line with the five-year average. Emilia-Romagna remains stable, with growth in Romagna offset by declines in Emilia, especially in grape weight. Central Italy shows a decline (-3%), where gains in Umbria (+10%), the Marche (+18%), and Lazio (+5%) are not enough to offset Tuscany’s drop (-13%), which is considered to be physiological after an exceptionally abundant 2024.

Although still exposed to weather conditions in the coming weeks, Assoenologi, Uiv, and Ismea explain that the grapes are in good health, thanks to careful and scientific agronomic management, essential in a context which is increasingly affected by extreme weather events. The harvest campaign was preceded by a period of uncertainty due to summer climate variability. However, good water reserves accumulated during winter, a mild spring, and an early but fluctuating summer have fostered an early harvest in many areas with a timeline expected to be long, especially in southern regions. Phenolic ripeness achieved in most areas, combined with aromatic potential boosted by late August temperature swings, suggests fresh and long-lived wines in the North, clean and balanced profiles in Central Italy, and structured, characterful reds in the South. Growth is clearly driven by the South, where production is expected to rise by double digits (+18%). Southern regions responded well to the heatwaves in June and August, thanks to water reserves built up in spring. In Puglia (+17%), production is up compared to last year, with healthy grapes and good balance; particularly, red grapes show strong phenolic maturity. Strong recovery also in the Abruzzi (+25%), as well as in Molise (+25%). The situation is different in Sicily (+20%), but it is clearly rebounding from last year’s drought-related challenges. The outlook is positive across other southern regions with Campania (+13%) where one has high expectations for late-ripening varieties which benefited from moderate temperatures in late August. Basilicata (+40%) and Calabria (+15%) show varied conditions depending on the area, but without widespread issues. Only Sardinia remains stable compared to last year, due to heat and irregular rainfall.

Northern Italy also shows production growth, although significantly more modest than in the South. In the Northwest, rainy spring conditions supported good vegetative development, while summer heatwaves did not compromise grape health. The largest estimated increase is in Lombardy (+15%), followed by more limited growth in Piedmont (+5%), and Aosta Valley (+8%). Liguria remains stable.

The Northeast presents a quite varied picture, with vineyards experiencing a very rainy spring which required careful disease management. Summer was inconsistent, with periods of intense heat followed by occasional storms, sometimes intense. In this area, Friuli-Venezia Giulia shows the highest estimated increase (+10%), followed by South Tyrol (+9%), while the growth of Veneto is minimal (+2%). Emilia-Romagna remains stable, with growth in Romagna offset by declines in Emilia, especially in grape weight.

Central Italy shows a negative trend (-3%), as strong increases in Umbria (+10%), the Marche (+18%), and Lazio (+5%) fail to offset the decline of Tuscany (-13%), which is considered to be physiological after an exceptionally abundant 2024.

Balancing what appears to be an excellent vintage overall, despite regional differences, there is a particularly complex market scenario. As said, both domestic and global demand are declining, influenced by emerging consumption models that the wine sector is beginning to address to. The 2024/2025 campaign, explain Uiv, Ismea, and Assoenologi, closed with a slight increase in wine prices with Ismea Producer Price Index registering an overall +1%, though trends vary across segments: table wines rose by 4% thanks to white wines, while red wines declined; Doc-Dcg marked a -2% due to red wines, with a slight increase in whites; while Igt wines rose by +1%, equally distributed. A situation analysis shows that during the summer months, price lists declined waiting for the new campaign and the evolution of international production, which affects table wines most, while Doc-Docgs follow more independent dynamics.

Wine stocks, up to July, 31st, 2025 remain stable compared to the previous year (Cantina Italia data). On the domestic demand front, Gdo shows growth in sparkling wine purchases, both in volume and value, while still wines are slowing down (Ismea/Nielsen IQ data). Regarding foreign demand, after a positive 2024, the first five months of 2025 confirm the achieved value levels with a slight drop in volumes (-4%) due to a decline in shipments of generic wines, while Pdo wines show an increase.

In short, as the 2025 harvest progresses, cellars are filling up more than emptying, and the challenge will be to find a market for such a large production trying to maintain price levels, mainly for lower-value wines, and it will be anything but easy.

Copyright © 2000/2026

Contatti: info@winenews.it

Seguici anche su Twitter: @WineNewsIt

Seguici anche su Facebook: @winenewsit

Questo articolo è tratto dall'archivio di WineNews - Tutti i diritti riservati - Copyright © 2000/2026

")

")

. Stable volumes (-0.2%)")

")

")

")

2026")

")

")

")

- La Selvanella 2025 (300x250)")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")