acquires vineyards of Domaine Lumineux")

Saturday 28th of March 2026 - Last Update: 22:57

")

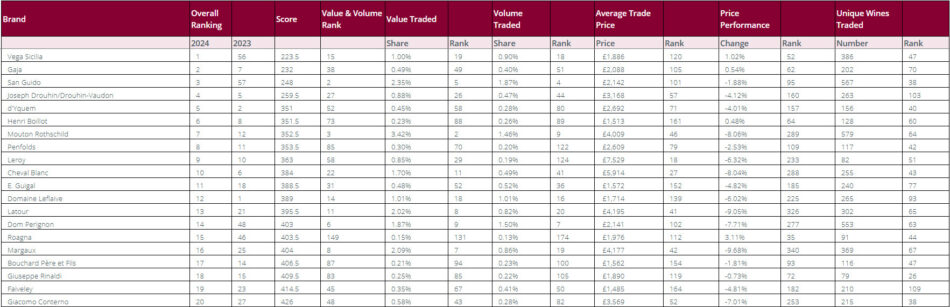

In a 2024 of great difficulty for the fine wines market, after a 2023 already in sharp decline after years of important growth, Italy, which does not soar but defends itself better than others, gains prestige and authority with its most prestigious labels. Testifying to this is the “Liv-Ex Power 100” 2024, just published, with Italy being able to celebrate with a double podium, because if at no. 1 there is the exploit of Vega Sicilia, one of the most famous wine brands of Spain and the world, deeply linked to the production area of the upper valley (Castile and León) of the Duero River, protagonist of a leap of no less than 55 positions, at no. 2 there is Gaja, an icon of Langhe and the first Italian brand in the ranking, once again (in 2023 it was at No. 7 and in 2022 at No. 38, demonstrating a climb, continuous, important) and, at No. 3, Tenuta San Guido, the cradle of “Sassicaia”, of the Incisa della Rocchetta family, the most renowned expression of Bolgheri. San Guido climbing 54 positions for another result that demonstrates the value of an iconic wine. Gaja, Liv-Ex points out, proved to be a counter-trend example because in a “market that has collapsed in the last two years”, the prestigious label climbed the ranking. A brand, Gaja’s, “built with care and consistency over decades, well known and reliable”. A detail that “is reflected in the breadth of wines marketed with 70 vintages of 13 different labels that have changed hands in the last 12 months”. A value also confirmed by the fact that it is “one of the 11 brands in the Power 100 whose average price has not fallen in the last year.” Sassicaia, on the other hand, is described by Liv-Ex as “a safe bet in a down market”, pointing out that “Sassicaia 2020 was the third most traded wine in value and the eighth most traded in volume during the period considered for the Power 100”.

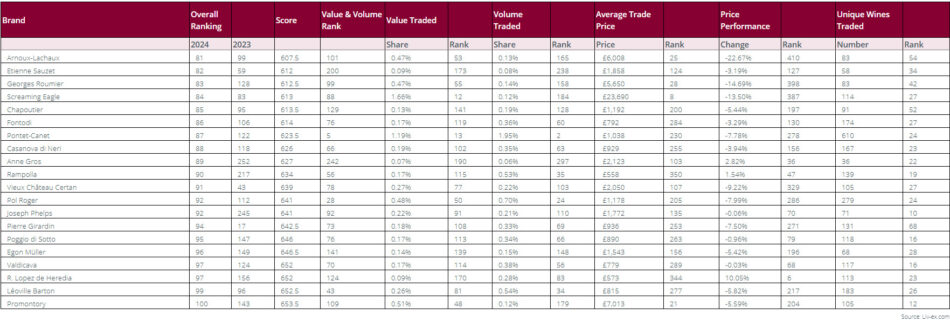

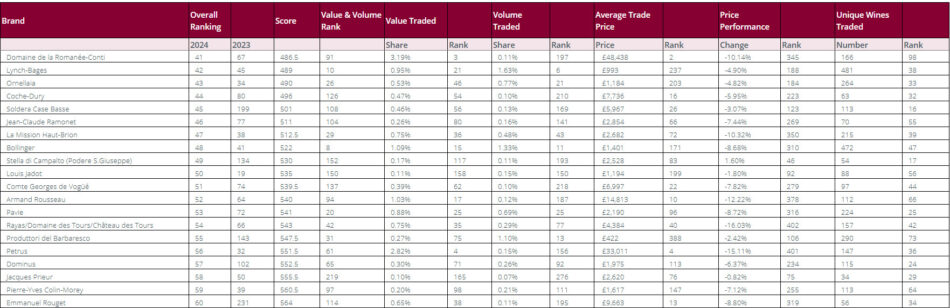

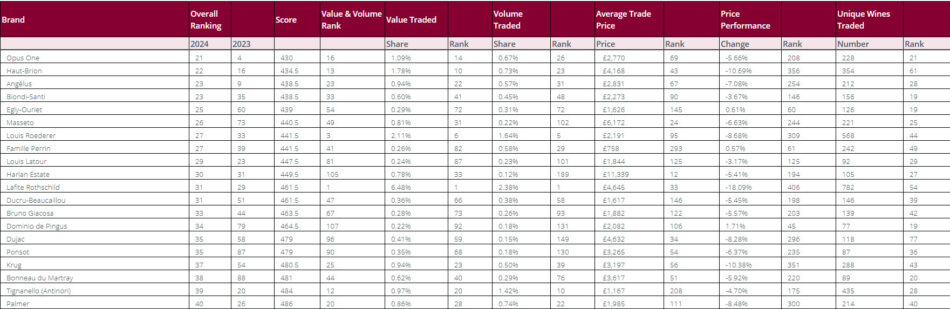

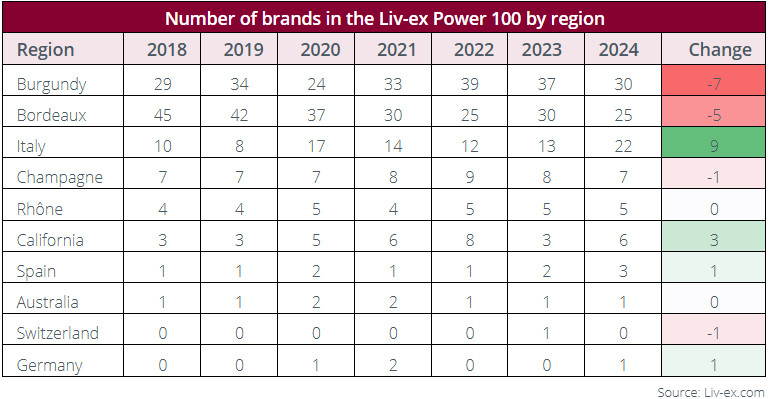

The “revolution” in the Top 10 continues alternating, however, with confirmations such as, from Burgundy, Joseph Drouhin/Drouhin Vaudon at No. 4 (was at No. 5 in 2023), Chateau d’Yquem (Bordeaux) moving from No. 2 to No. 5, Henri Boillot (Burgundy) at No. 6 (up from No. 8), Mouton Rothschild (Bordeaux) at No. 7 (to No. 12 in 2023), Penfolds (Australia) at No. 8 (+3 positions), Leroy (Burgundy) at No. 9 (-1 position on 2023), and Cheval Blanc (Bordeaux) slipping from No. 6 to No. 10. At the level of territories, Burgundy continues to be the leader with 30 labels but loses 7 from 12 months ago. Bordeaux has 25 (-5) while Italy, in third position, seals its own record with 22 labels, a good 9 more than 2023, with Tuscany scoring 9. total share, fifth overall, doing better than the 7.2% of 2023 and Piedmont right behind, and growing, with 4% (3.5 in 2023). Behind Gaja and Tenuta San Guido, among the top Italian brands, is Roagna, one of the top-rated and benchmark names in the Piedmontese appellation, at No. 15 (No. 46 in 2023). Preceding the Barolo griffe Giuseppe Rinaldi at position No. 18 (was No. 15 in 2023), while Giacomo Conterno “the house of Barolo Monfortino” rises to No. 20 (was No. 27). Also continuing to grow is Biondi Santi, cradle of Brunello di Montalcino and now of the Descours Family’s Epi Group, at No. 23 (it was at No. 35 in 2023 and even at No. 134 in 2022). A significant leap is also that of Masseto, Frescobaldi’s jewel, at No. 26 (it was at No. 73), and Bruno Giacosa, another spearhead of Piedmont winemaking, also rises to No. 33 (up from No. 44 in 2023).

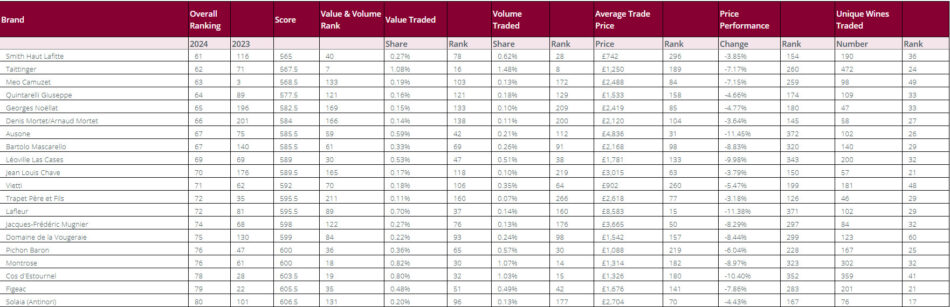

In the Top 40, at No. 39, is Antinori’s Tignanello (at No. 20 in 2023), in a year in which one of Antinori’s jewel labels, celebrating 50 years since its first release on the market (with the 1971 vintage, in 1974, also celebrated by an exceptional auction, for the first time ex cellar, auctioned by Christies’s) has conquered top positions of international “Top 100” such as that of “Wine Spectator” and that of “Vinous” by Antonio Galloni. Again, position No. 43 for Ornellaia of the Frescobaldi Group (No. 34 in 2023) and sensational climb for Soldera Case Basse, one of the highest and most “sought-after” expressions by collectors of Montalcino wines, which goes from No. 199 to No. 45, the biggest “jump” among Italian producers. But this is not the only exploit coming from Montalcino, because at No. 49 is Stella di Campalto (at No. 134 in 2023) while a brilliant result is also signed by the Produttori del Barbaresco cooperative at position No. 55 (it was at No. 143 in 2023). On the rise is another big name in Italian wine, Giuseppe Quintarelli, icon of Valpolicella at No. 64 (No. 89 in 2023) and Bartolo Mascarello, historic winery in Barolo, at No. 67 (No. 140 in 2023). It remains in the Langhe with the Vietti griffe at No. 71 (No. 62 in 2023), while another excellence of Tuscany, Antinori’s Solaia, comes in at No. 80 (No. 101 in 2023), and that, therefore, beats, with this supercelebrated label, the Tignanello, which, as already written, is in position No. 39. One of the most important griffes of Chianti Classico, on the other hand, such as Fontodi, is placed at box No. 86 (No. 106 in 2023), while Casanova di Neri, among the references of Brunello di Montalcino, is at No. 88 (No. 118 in 2023). And, again in Tuscany, but still on the Chianti Classico side, Rampolla marks its entry into the top 100 at No. 90 (No. 217 in 2023). Brunello di Montalcino closes out the last two Belpaese names in the “Liv-Ex Power 100” with Poggio di Sotto (ColleMassari Group) at No. 95 (No. 147 in 2023), and Valdicava at No. 97 (No. 124 in 2023).

Italy, the Liv-Ex report points out, stands out for achieving the highest results in the 2024 Power 100, occupying 22 places, 9 more than last year, now on the “heels” of Burgundy and Bordeaux. And if Tuscany, and in particular the terroir of Montalcino, achieved the greatest position gains, a closer look reveals a heterogeneous set of Italian producers who made this year's list, demonstrating a lively wine scene where homogeneity lies in the quality of the proposal. More delicate is the discourse regarding France: for Liv-Ex, as last year, Bordeaux “certainly remains the best and most widely understood option: the mechanisms have remained unchanged and liquidity is still its strong point. However, in the current market, it is not necessarily the safest bet, particularly for recent vintages that have collapsed due to release prices virtually across the board”. Burgundy, on the other hand, while remaining the queen in the Power 100, is a “victim of its own success” for Liv-Ex. Given the high volumes and affordable prices that characterized the biggest rises in 2024, it is not surprising that Burgundy has fared poorly this year. This is reflected in the Burgundy 150 index, which has fallen 14.7% in the past year and 27.8% since its peak in October 2022”. On a general level, the 2024 fine wines market, Live-Ex points out, “was characterized by two trends. First, activity has remained high: the number of wines traded has remained steady. We see this in the “Power 100”: the transaction count for the 2024 list is 7.9% higher than for the 2023 list. Second, buyers tend to be reluctant to buy quantities of bottles that they cannot move quickly, resulting in a -6.5% drop in traded volumes”. The conclusions highlight how “as confidence has receded from the market, players have turned to brands that represent the least risky bets”. But while last year the biggest certainty seemed to be “Bordeaux, this year it is brands that share many of its traits, but not its terroir, that have risen to the top. Volume, liquidity, historic branding and prices that invite you to pop the bottles are their calling cards. And, as the market is still looking for a turning point, this course is unlikely to change in the short term”.

Copyright © 2000/2026

Contatti: info@winenews.it

Seguici anche su Twitter: @WineNewsIt

Seguici anche su Facebook: @winenewsit

Questo articolo è tratto dall'archivio di WineNews - Tutti i diritti riservati - Copyright © 2000/2026

")

")

")

2026")

")

")

")

- La Selvanella 2025 (300x250)")

")

")

")

")

2026 (300x120)")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")