Wednesday 5th of August 2026 - Last Update: 13:14

")

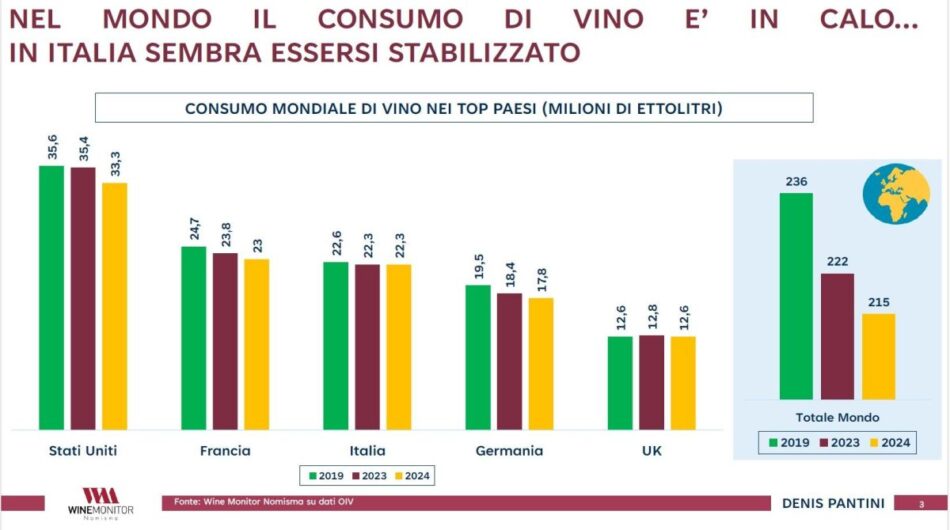

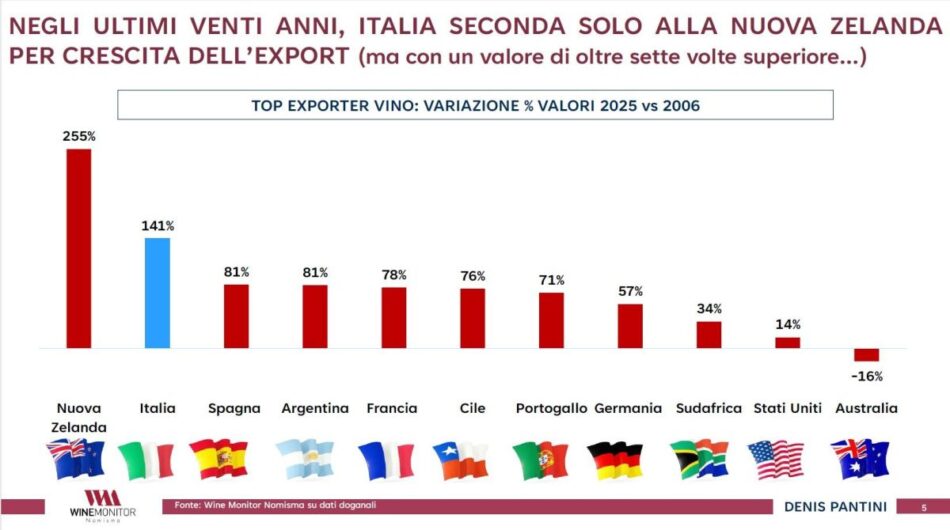

Italian wine is holding its ground, but changing its skin: while global consumption declines and domestic consumption stabilizes without showing growth, the sector increasingly relies on exports and on a profound transformation in consumer habits, influenced by health awareness, new generations, and the search for territorial identity. According to an analysis by Denis Pantini, head of the Nomisma Wine Monitor Observatory, presented in recent days at the Wine Market Forum held at the Accademia Intrecci in Castiglione in Teverina, promoted by the Chiasso-Cotarella Wine Consulting Firm, the global landscape shows a contraction in wine consumption, which dropped from 236 to 215 million hectoliters between 2019 and 2024. Italy, meanwhile, shows substantial stability (from 22.6 to 22.3 million hectoliters), though this masks structural weaknesses, beginning with the country growing dependence on foreign markets: over the last 20 years, Italian wine exports have grown in value by +141%, second only to New Zealand (+255%), but with an economic value more than 7 times higher. This growth has compensated for the decline in domestic consumption (-18% in volume, compared to a -6% drop in production, which didn’t collapse thanks to a +37% increase in exports).

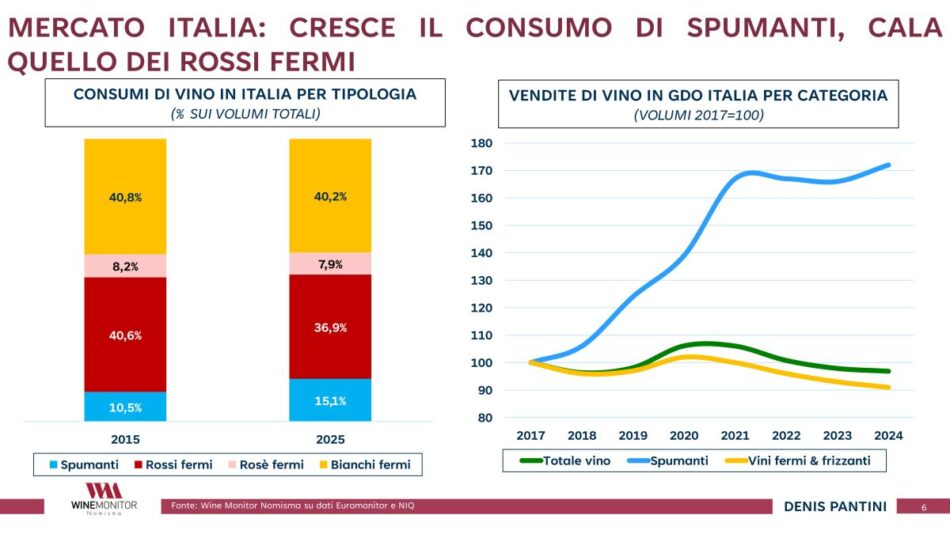

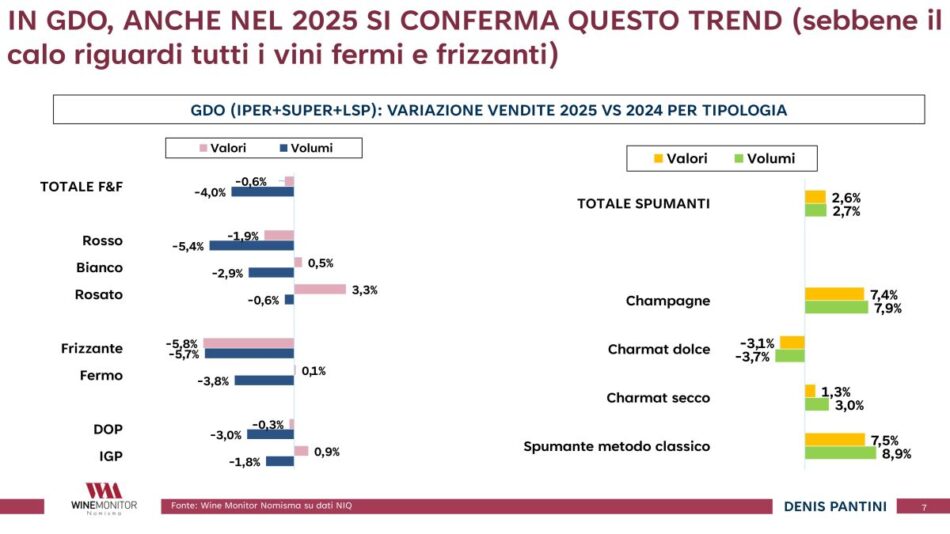

On the domestic front, changing consumption habits are clear in preferences: sparkling wines reached more than 15% of consumption in 2025 (compared to 10.5% in 2015), while still red wines have dropped to 36.9% (from 40.6% ten years ago). This signals a demand shifting toward fresher, lighter, and more versatile products, with white wine consumption remaining stable (40.8% vs. 40.2%). This trend is confirmed by wine purchases in gdo in 2025, where still and semi-sparkling wines declined (-0.6% in value and -4% in volume), while sparkling wines increased (+2.6% in value and +2.7% in volume). Looking at consumption channels, out-of-home consumption now accounts for 30% of total volume, slightly down from 10 years ago.

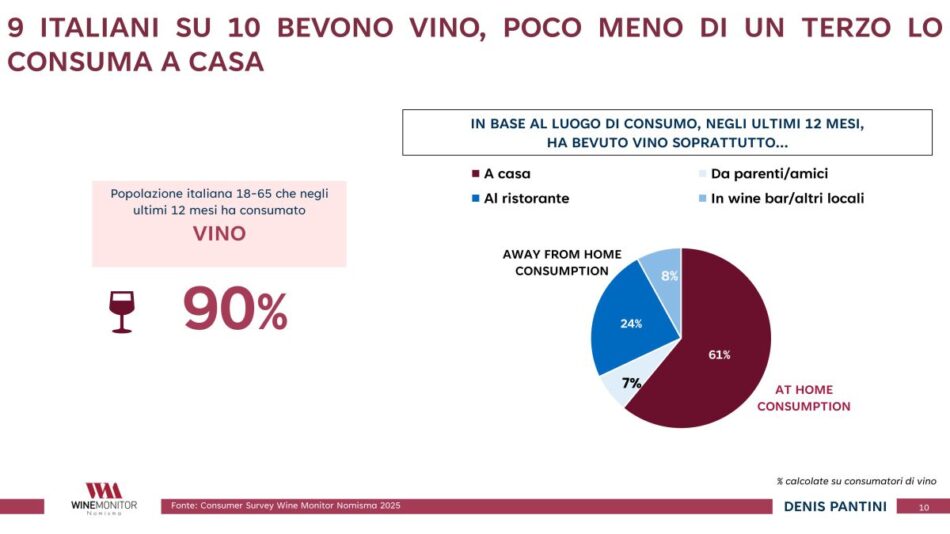

The main drivers behind the decline in consumption include greater attention to physical well-being and health (32%), fear of penalties related to traffic regulations (25%), sobriety (15%), dieting and economic savings (14%). Despite this, 9 out of 10 Italians drank wine in the past year, 61% at home, 24% at restaurants, 8% in wine bars and similar venues, and 7% with relatives or friends. However, consumption modes and frequency are changing, with a reduction in habitual consumers among younger age groups and a shift toward occasional consumption.

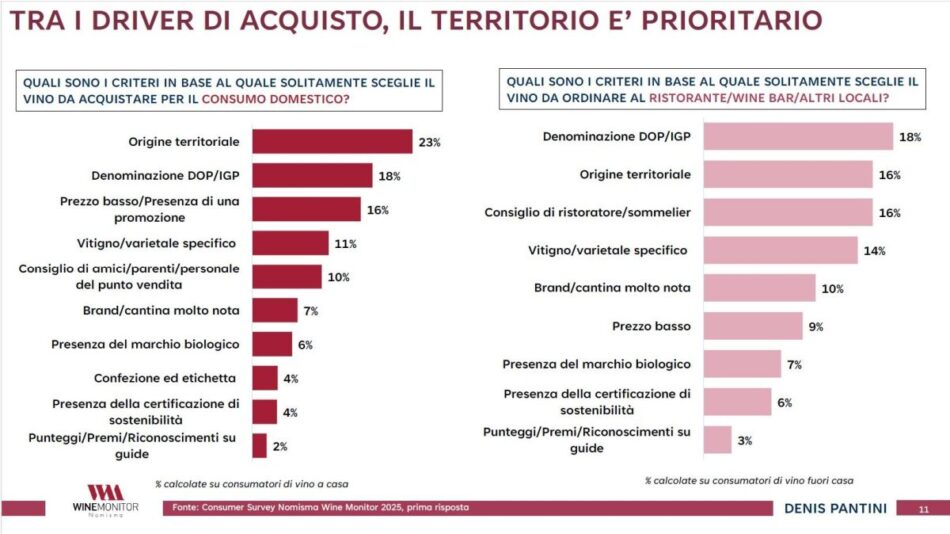

Territory is the primary driver of wine choice, both at home and out-of-home, confirming that the connection with the place of production is perceived as a guarantee of quality, authenticity, and reliability: for home consumption, geographical origin ranks first (23%), followed by PDO/PGI designation (18%) and low price or promotions (16%). In out-of-home consumption, PDO/PGI designation becomes more important (18%), followed by origin (16%) and recommendations from restaurateurs or sommeliers (16%). Trusted intermediaries - restaurateurs, sommeliers, but also friends and family - play a key role in guiding choices, while price remains relevant but not dominant, signaling a consumer increasingly willing to recognize value. At the same time, modern drivers such as sustainability and organic certification are gaining ground. At the bottom of the list, there are scores, awards, and guide ratings.

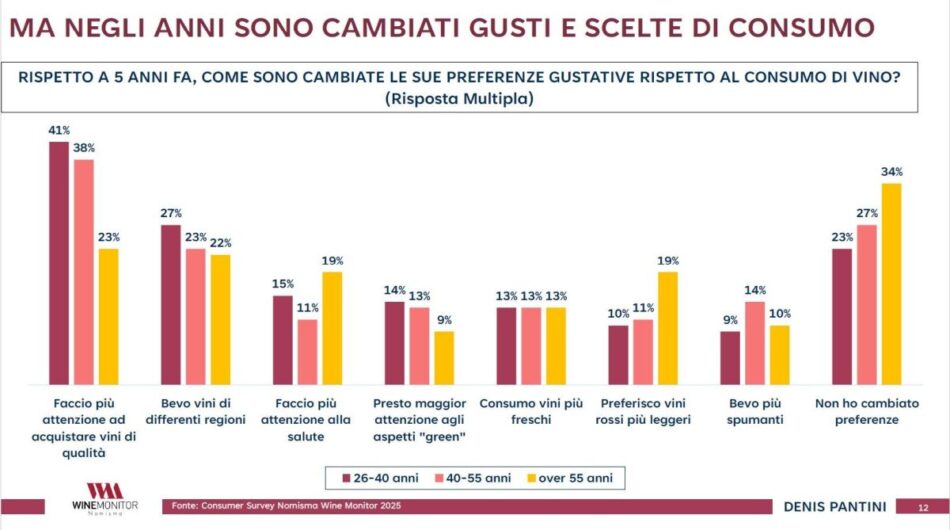

These transformations become even more evident when examining taste evolution: compared to 5 years ago, a significant share of consumers aged between 26 to 40 years old declare that they pay more attention to quality (41%), explore wines from different regions (27%), and place greater emphasis on health-related aspects (15%) and sustainability (14%). This translates into a growing preference for fresher, lighter, and more versatile wines - consistent with the rise of sparkling wines and the repositioning of reds toward less structured styles - as well as a decline in daily consumption, increasingly replaced by selective and conscious drinking occasions.

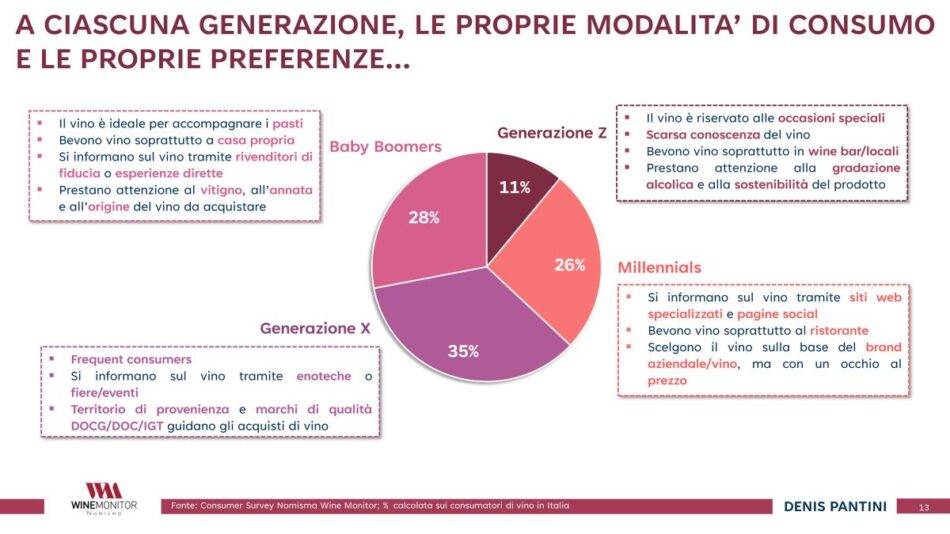

The real turning point, however, lies in generational identity, which is redefining the market. Gen Z, currently only 11% of wine consumers, shows a still fragile relationship with the category: they mainly consume wine out of home, in informal settings such as wine bars and trendy venues, get information through social media and digital platforms, and choose recognizable but accessible brands, with attention to alcohol content and sustainability. Millennials (26%) represent the core of current consumption: they are frequent consumers, attend fairs and events, rely on wine shops and specialized channels, and look for a balance between quality, territorial origin, and price. Generation X and Baby Boomers maintain a more traditional approach: wine is an integral part of home meals or associated with special occasions, and choices are based on established knowledge (grape variety, vintage, denomination) and trusted relationships with retailers or producers.

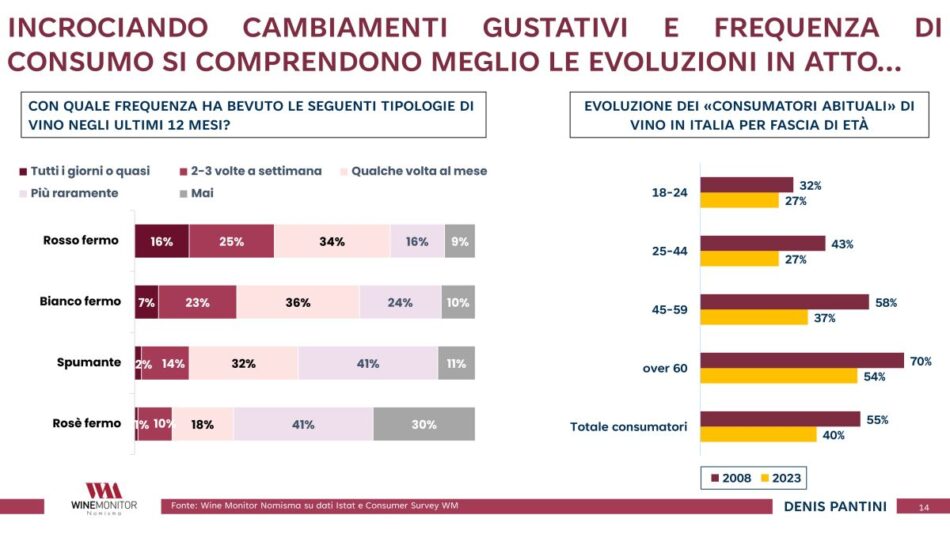

Cross-referencing age and frequency of consumption reveals another key element: between 2008 and 2023, habitual consumption declined among younger age groups and concentrated among older ones. This phenomenon intertwines with the structural issue of the “demographic winter”: in the coming decades, the Italian population is projected to shrink and age, with the over-60 group reaching 40.9% in 2055 and a significant contraction in younger age groups. The sector faces a twofold risk: on the one hand, a potentially smaller consumer base; on the other hand, a reduced ability to ensure generational turnover in consumption.

Copyright © 2000/2026

Contatti: info@winenews.it

Seguici anche su Twitter: @WineNewsIt

Seguici anche su Facebook: @winenewsit

Questo articolo è tratto dall'archivio di WineNews - Tutti i diritti riservati - Copyright © 2000/2026

")

wine. Us Wine Trade Alliance analysis")

")

")

")

")

")

")

2026")

")

")

")

- La Selvanella 2025 (300x250)")

")

")

")

")

")

2026 (300x120)")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")