Wednesday 22nd of July 2026 - Last Update: 18:18

")

If historical markets are slowing while emerging ones are growing, diversification has now become a must for the future of Italian wine exports (making the most of new European free trade agreements), just as, in the domestic market, the youth challenge is decisive in countering the decline in sales linked to the drop in both the number of consumers and the frequency of consumption. The speech by Denis Pantini, Head of Nomisma Wine Monitor, today, at the Assoenologi Congress No. 79 in Conegliano, in the heart of the Conegliano Valdobbiadene Prosecco Superiore DOCG hills (a Unesco World Heritage site), presented a mixed picture of the performance of the Italian wine market, identifying opportunities to work on in order to reverse a negative trend that can (and must) be managed.

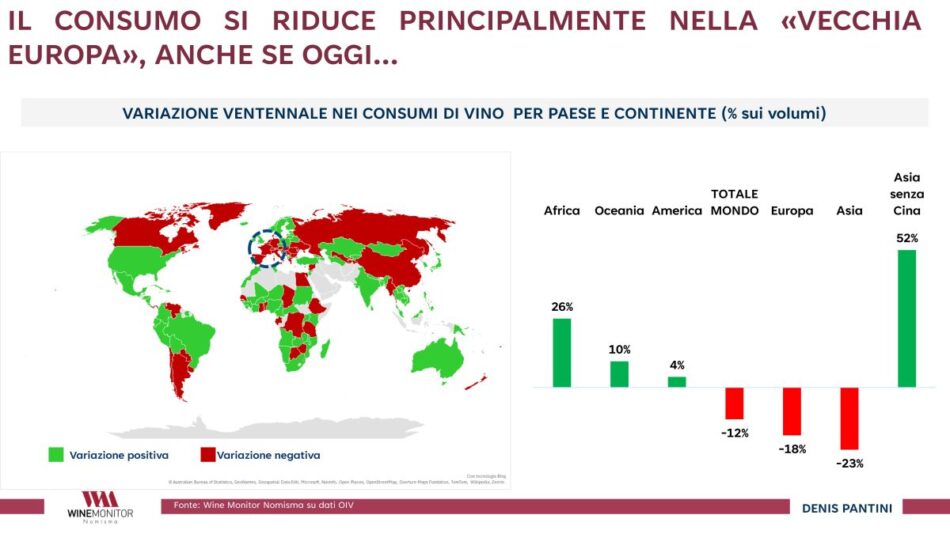

In a global picture over the last twenty years which, after uninterrupted growth up to the 2017 peak, saw both global imports fall in 2025 (down to 110 million hectoliters) and consumption decline (to 208 million), it clearly emerges that the traditional markets where the greatest consumption declines have been recorded are Europe (-18%) and Asia, dragged down by China (which, excluding the “Dragon Country”, would instead show +52%), compared to other geographical areas that show positive trends (Africa +26%, Oceania +10%, even if with a low share of total consumption, and the Americas with an overall +4%).

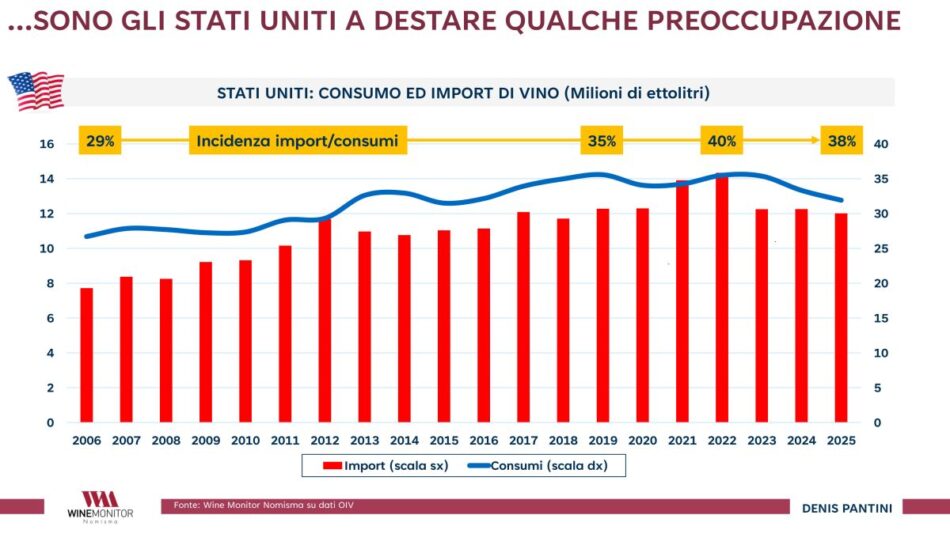

“Figures which show how the geography of wine is changing its skin - said Pantini - and that is where the supply chain must start looking with renewed interest and attention”. What concerns analysts most, of course, is the slowdown in the United States, which remains the world leading market with more than 33 million hectoliters of domestic consumption (12 million hectoliters of which are imports). Although the last three years have recorded a significant decline, historical analysis shows that the American market has already experienced similar cycles, such as in 2014-2015, with the difference that today the reduction in consumption is also affecting domestic production. Twenty years ago only 3 out of 10 bottles consumed in the U.S. were of foreign origin; today it is 4 out of 10, with imports holding steady (38% of sales in 2025), while local producers are suffering.

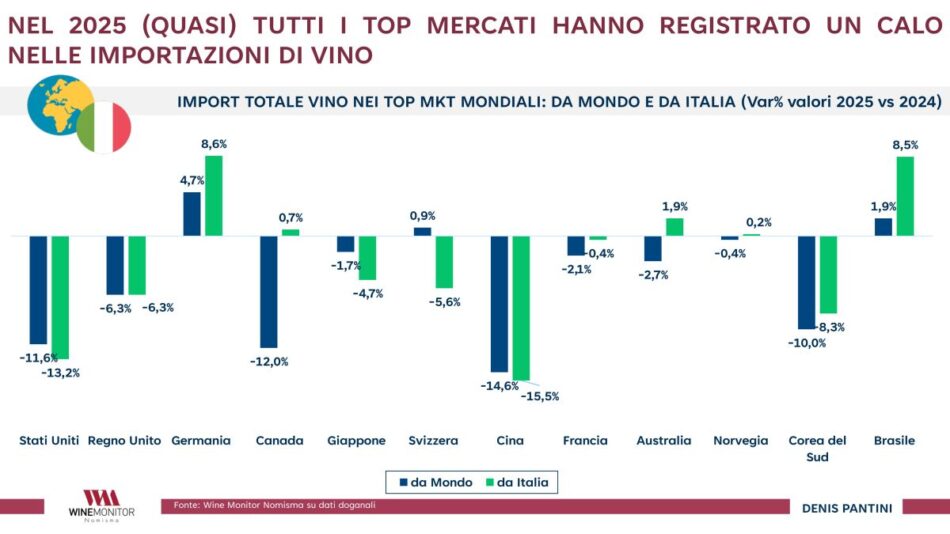

In the overall balance for 2025, however, almost all international markets recorded declines. In the U.S., for example, Italian wine posted -13% (compared to a general import decline of -11.6%); in Germany, by contrast, Italy performed better than the global average (+8.6% vs +4.7%), as well as in Canada (+0.7% Italy vs -12%) and in Brazil (+1.9% vs -8.5%).

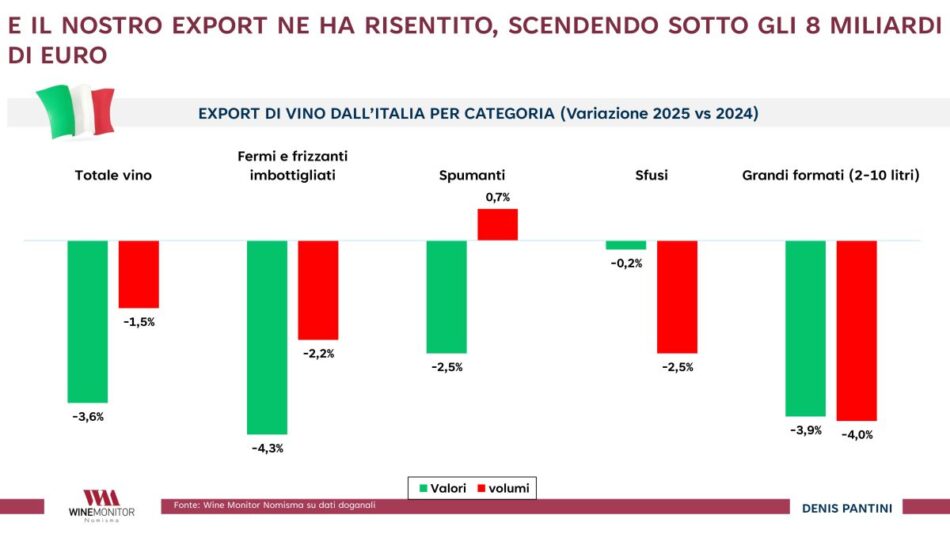

These diversified trends are nonetheless affected by the overall global contraction, with a direct impact on our exports which, after exceeding the historic threshold of 8 billion euros in 2024, stood at 7.8 billion euros in 2025 (-3.6%), with reductions affecting all categories: bottled still and semi-sparkling wines (-4.3% in value and -2.2% in volume), sparkling wines (-2.5% in value and +0.7% in volume), bulk wine (-0.2% in value and -2.5% in volume), and large formats (-3.9% in value and -4% in volume).

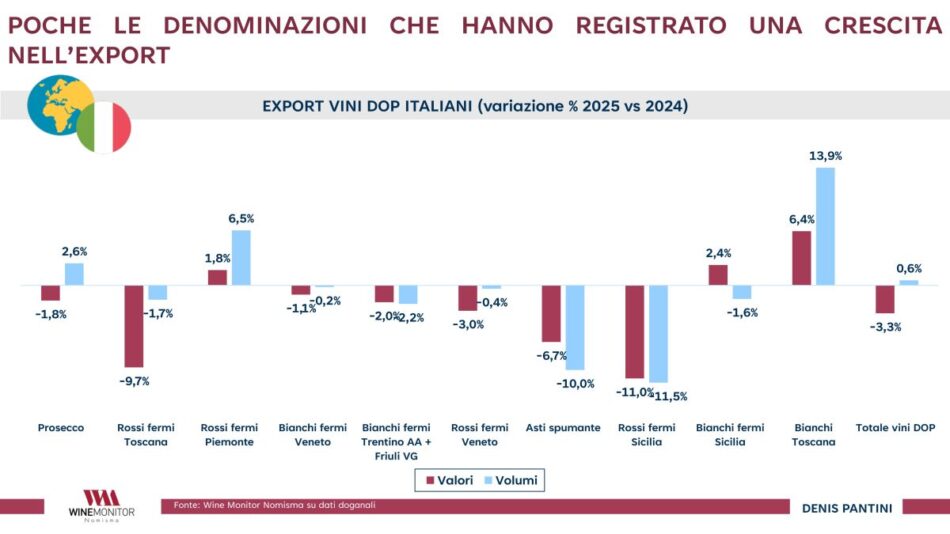

At the denomination level, dynamics are mixed: after 10 years of uninterrupted growth, Prosecco loses some value (-1.8%) while holding in volume (+2.6%); Tuscan red wines also slow down (-9.7% in value and -1.7% in volume), while Piedmont red wines perform well (+1.8% in value and +6.5% in volume), Sicilian still white wines (+2.4% in value and -1.6% in volume), and Tuscan Pdo white wines show an excellent performance (+6.4% in value and +13.9% in volume).

The most worrying overall figure in the current scenario concerns the reduction in value (total Pdo -3.3% vs +0.6% in volume). The drop in exports is mainly linked to a contraction in average prices, a reshaping of the export mix, or the need to sell the same product at more competitive prices.

But if “Athens weeps, Sparta doesn’t laugh”, commented Pantini, because looking at international competitors, Italy is the country which has best limited the damage: New Zealand shows a slight decline, stopping at -5% compared to 2024; Australia collapsed by 14.6%, paying the price for renewed difficulties in the Chinese market after the end of 220% tariffs; nearby competitors are also suffering (France -4.4% and Spain -5.1%), with the U.S. ending its export performance with a heavy -36%. The latter figure is the direct consequence of Donald Trump protectionist policies: retaliatory tariffs by key markets such as Canada and China have effectively wiped out American wine export channels.

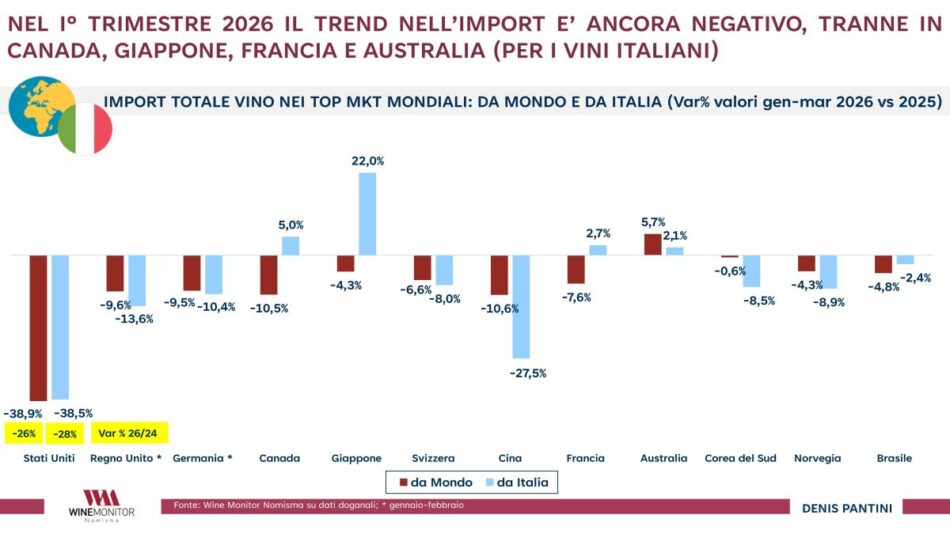

And, in the first quarter of 2026, the trend remains complex. Compared to the same period in 2025, there is a structural decline close to -40% in the U.S. market, a figure distorted by a rush to stockpile at the beginning of 2025 to avoid tariffs (but compared to 2024, the drop is around -30%). There is, however, a strong recovery in Japan (+22% imports from Italy) and Canada (+5%), while China (-27.5%) remains in a phase of deep recession.

But new growth opportunities can be found. “We must work on increasing the share of exports relative to production - stressed again Pantini - Italy currently exports about 40-45% of its wine, and reaching Australia target (which exports 58% of its production) is a realistic goal, without necessarily chasing the extreme model of New Zealand (98%), a country with a small population entirely focused on foreign markets”.

Starting with greater investment to open up to non-traditional markets, which are those with the highest growth rates. If until 2014 traditional markets (over 100 million euros per year) accounted for 85% of our exports, today they have dropped to 80%, while others, although small and fragmented, have grown by 30% (from 15% to 19.5%), showing very high development potential. Analysts identified about ten emerging markets by cross-referencing the historical growth of Italian wine imports with Imf Gdp forecasts up to 2030 and population size. This new geopolitical map focuses on three macro-areas: Eastern Europe and Central Asia (Poland, Romania, the Czech Republic, and Kazakhstan); Asia and the Far East (South Korea and Thailand); and Latin America (from Mexico to Colombia).

However, the areas affected by the most recent EU free trade agreements are those prioritized for development. In the Mercosur countries, a market of 260 million inhabitants and 3,000 billion euros in Gdp, where wine imports have grown by 145% in five years, the elimination of tariffs over the next seven years will offer good growth prospects for Italian wines (which currently hold an 8% share, with Tuscan reds leading Brazilian consumer preferences), although Chile dominates the area thanks to zero tariffs. Then, India (1.47 billion inhabitants and 3,800 billion euros Gdp), a very long-term challenge with still very low consumption and imports (about 25 million euros in total, dominated by Australia), but where Italian exports already account for 10% of market share, driven by the success of Prosecco. Finally Australia (28 million inhabitants and 1,850 billion euros Gdp), where the recent free trade agreement opens the door to a country with one of the highest per capita incomes in the world, offering a new commercial outlet in a market still driven by Prosecco.

On the domestic front, the challenge lies in building loyalty among younger generations, preventing their gradual distancing from the world of wine by capturing their new consumption styles. The Italian market in 2025 fell from 22.3 to 20.2 million hectoliters, showing a structural shift toward sparkling wines: whereas in 2015 only 11 out of 100 wines consumed in Italy were sparkling, today the figure is 15 out of 100, a growth parallel to the decline in red wines (which have dropped from 41% to 37% of total consumption), while rosé wines stand at 7% and still whites maintain a stable share below 40%.

With the boom in large-scale retail sales recorded during the 2020 lockdown now over, the domestic market continues to shrink in volume. The only notable exception is Metodo Classico, which, although accounting for 10% of the sparkling category, grew by 25% in volume (+17.5% in value) in the first quarter of the year.

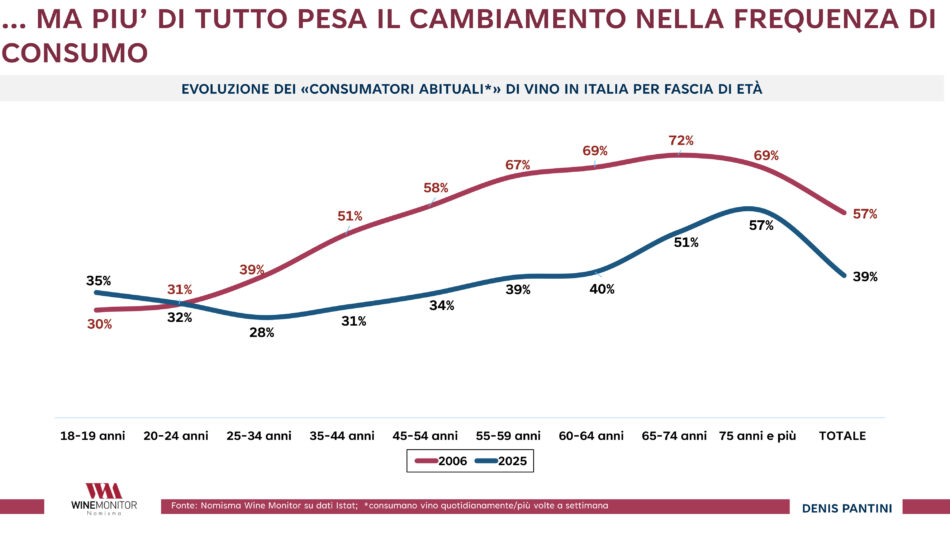

But, the real strategic issue for the future of the sector is the deep demographic and consumption habit changes underway in Italy. Istat estimates for 2035 foresee the Italian population dropping below 58 million, a sharp decline from the peak of over 60 million reached in 2015. The consumer base is progressively aging, with constant growth in the over-65 segment, accompanied by a collapse in regular consumption rates over the past 20 years. While among young people up to 24 the impact of the crisis is smaller, since their initial approach has historically been linked to occasional consumption, the gap has widened dramatically among those aged 35 to 50, where regular consumers have dropped from 50-60% in 2006 to 30-35% today.

This shift indicates a phase of abandonment (decline?) of the traditional Mediterranean model, which considered wine as a daily beverage closely tied to meals. Today, consumption is concentrated almost exclusively on weekends and in isolated social contexts, opening another serious issue, concluded Pantini: if the Italian model shifts toward occasional consumption and weekend excesses, will the sector risk losing its historic hallmark of conscious and moderate consumption?

Copyright © 2000/2026

Contatti: info@winenews.it

Seguici anche su Twitter: @WineNewsIt

Seguici anche su Facebook: @winenewsit

Questo articolo è tratto dall'archivio di WineNews - Tutti i diritti riservati - Copyright © 2000/2026

: Boscarelli, one of Vino Nobile tops, invests in future")

")

in 2026 Top 20 performers")

")

")

")

")

")

")

")

2026")

")

")

")

- La Selvanella 2025 (300x250)")

")

")

")

")

")

2026 (300x120)")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")