Friday 20th of March 2026 - Last Update: 19:23

")

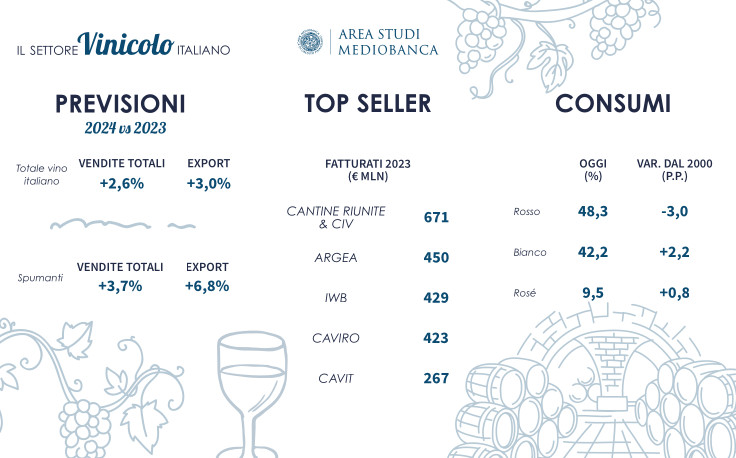

Major Italian wine producers expect overall sales growth of +2.6% for 2024, and +3% for exports. There is no let-up in optimism for sparkling wines (thanks to +3.7% in total revenues), especially across borders (+6.8% exports), while still wines are expected to grow +2.3% (+2.2% exports). After all, 2023 closed without significant changes (-0.2% on 2022) with a slight deterioration in the domestic market (-0.7%) compared to the foreign market (+0.3%), where the good performance of sparkling wines (+2.5%) stands out. Ebit margin reported an increase of 1.4% over 2022, with a ratio of net income to sales of 4.2%. And this despite a 4.5% decrease in quantities sold across all channels and inflation that eroded household purchasing power penalizing mid-range wines (-10.1% on 2022) confirming greater market polarization. Low-end wines declined slightly (-1.7%, with a market share of 44.2%), compared to an increasingly premium (+12.7% very high-end wines on 2022; market share of 18.6%) and sustainable market (+1.4% organic wines, 5.4% market share; +9.6% vegan wines, 2.7% market share, +1.8% natural wines, m.s. Of 1%). That’s according to the Survey on the wine sector in Italy by the Mediobanca Study Area, which covers 253 major Italian corporations with 2022 revenues of more than 20 million euros and aggregate revenues of 11.8 billion euros, or 88.4% of the sector’s national turnover, with a focus on PDO and PGI wines, major M&A deals and sustainability.

In particular, looking at the best-performing Italian companies, the sales leadership in 2023 remains with the Cantine Riunite-Civ group, with sales at 670.6 million (-3.4% on 2022). In second place is confirmed the Argea wine pole (449.5 million, -1.2%), followed by Iwb-Italian Wine Brands, with 429.1 million (-0.3% over 2022). Turnover 2023 is also above 400 million for the Romagna-based cooperative Caviro (423.1 million), up 1.4% on 2022. Seven companies note revenues between 200 and 300 million euros: Trentino cooperative Cavit (2023 turnover of 267.1 million euros, up 0.9% on 2022), Veneto-based Santa Margherita (255.4 million euros, -2%), Tuscany-based Antinori (250.3 million euros, +1.9%), La Marca, which specializes in sparkling wine production, with 2023 sales of 225.8 million euros (-4%), Piedmont’s Fratelli Martini (219.6 million, +1.1%), Trentino’s Mezzacorona (217.7 million, +2%), and the Collis Group, which expanded to 209.4 million euros, (+64.8% on 2022). Looking at profitability (ratio of net income to turnover), 2023 sees Tuscan Frescobaldi (29%) leading the way, followed by Veneto’s Santa Margherita (18.5%). Closing the podium is Antinori with a profit on sales of 17%, up 2.6 percentage points on 2022. Some companies have a very high export share, in some cases almost totalitarian: Fantini Group touches 96.4%, Ruffino 91.1%, Argea 89.9%.

Overall, looking at the world scenario, world wine production in 2023 is estimated at 237 million hectoliters, down sharply from 2022 (-9.6%). World consumption in 221 million hectoliters (-2.6%). The reshaping of demand, induced by generational change and the spread of health patterns as well as climate change, have caused a decline in red wine consumption from an average 51.3% share in the 2000-2004 period to 48.3% in 2017-2021. White wine consumption (from 40% to 42.2% +2.2 points) and rosé wine consumption (from 8.7% to 9.5%+0.8 points) bucked the trend. Italy follows the world trend recording -23.2% in production compared to 2022 and -1.6% in consumption, with 37.4 liters per capita per year. In surplus for Italy is the trade balance: in 20 years it has grown at an average annual rate of 5.5%, from 2.5 billion euros in 2003 to 7.2 in 2023. Italy is the leading wine exporter in quantity (21.4 million hectoliters in 2023) and the second in value (7.7 billion euros behind only France’s 11.9 billion).

Flagship, 47.7% of Italian wine is DOP (Doc and Docg) in 2023, up from 38.5% in 2013. Igp wines drop from 35% in 2023 to 27% in 2023, moving closer to table wines (25.3% in 2023). Taking the lion’s share are Piedmont with 19 Docg and 41 Doc, Tuscany (11 Docg, 41 Doc and 6 Igt) and Veneto (14 Docg, 29 Doc and 10 Igt). Tuscany concentrates 39.3% of PDO wine production; in Piedmont, 94.6% of regional production is PDO. Overall, the value of bottled PDOs and IGTs is 4.3 billion euros in Veneto, followed by Piedmont with 1.4 billion and Tuscany with 1.2 billion. Regional excellence drives companies’ financial statements: Tuscan companies get the highest Ebit margin (16.5%) and the best Roi (6.3%), Veneto and Piedmont in second position (both 6.1%). Tuscany also has the highest financial strength, with financial debt amounting to just 18.4% of invested capital. Major exporters were producers from Piedmont (64.5% of sales) and Tuscany (60.6%). In 2023 exports drove growth for companies in Friuli (+6.1% overall sales and +22.3% across borders), Lombardy (+4.4%; +7.4%) and Emilia-Romagna (+1.6%; +8.6%). Optimism for 2024 for Emilia-Romagna (+4.6%), Puglia (+4.3%) and Piedmont (+4.2%).

The “Identity Card” of enterprises, shows how family control is responsible for 64.8% of equity, a share that rises to 81.4% if cooperatives are also considered.

Financial investors participate in 10.9% of equity: banks and insurance companies (5.2%) are absent in smaller firms, while private equity funds (4.1% of equity) participate in the capital of major wine companies regardless of size. As size decreases, the incidence of non-Italian ownership also falls, at 7.6% of equity. The relationship with financial markets is negligible: only two companies have been listed on Aim since 2015 (Masi Agricola and Iwb).

Finally, sustainability is definitely in need of improvement: only 34.9% of the largest Italian wine companies draw up a Sustainability Report (38.6% of producers with more than 50 million in turnover). The main reasons are the complexity of the validation or accounting process (for 26.8% of companies), lack of benchmarks or reference best practices (14.3%) difficulty in involving relevant business functions and lack of specific skills (10.7%).

Copyright © 2000/2026

Contatti: info@winenews.it

Seguici anche su Twitter: @WineNewsIt

Seguici anche su Facebook: @winenewsit

Questo articolo è tratto dall'archivio di WineNews - Tutti i diritti riservati - Copyright © 2000/2026

")

")

")

")

. Stable volumes (-0.2%)")

")

")

")

2026")

")

")

")

- La Selvanella 2025 (300x250)")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")